Best Of The Best Tips About Finance Lease Accounting Ifrs 16 What Goes On The Income Statement And Balance Sheet

Finance Lease Journal Entries Ifrs 16 Financeinfo P&l And Bs Biological Assets In Balance Sheet

Ifrs 16 Leases Youtube Balance Sheet Reconciliation Means Trial To Final Accounts

Car Rental Financial Statements Condensed Balance Sheet Example 3

Accounting For Impairment Of Lease Receivables Under Ifrs 9 Gaap Dynamics Prepare Statement Profit And Loss Interest Income In

Ifrs 16 Cash Flow Statement Financial Huupgames Provision For Doubtful Debts Income And Fund Ppt

Ifrs 16 Lessor Accounting Operating Lease Cima F2 Youtube Deferred Credits Will Appear On The Balance Sheet With Net Assets

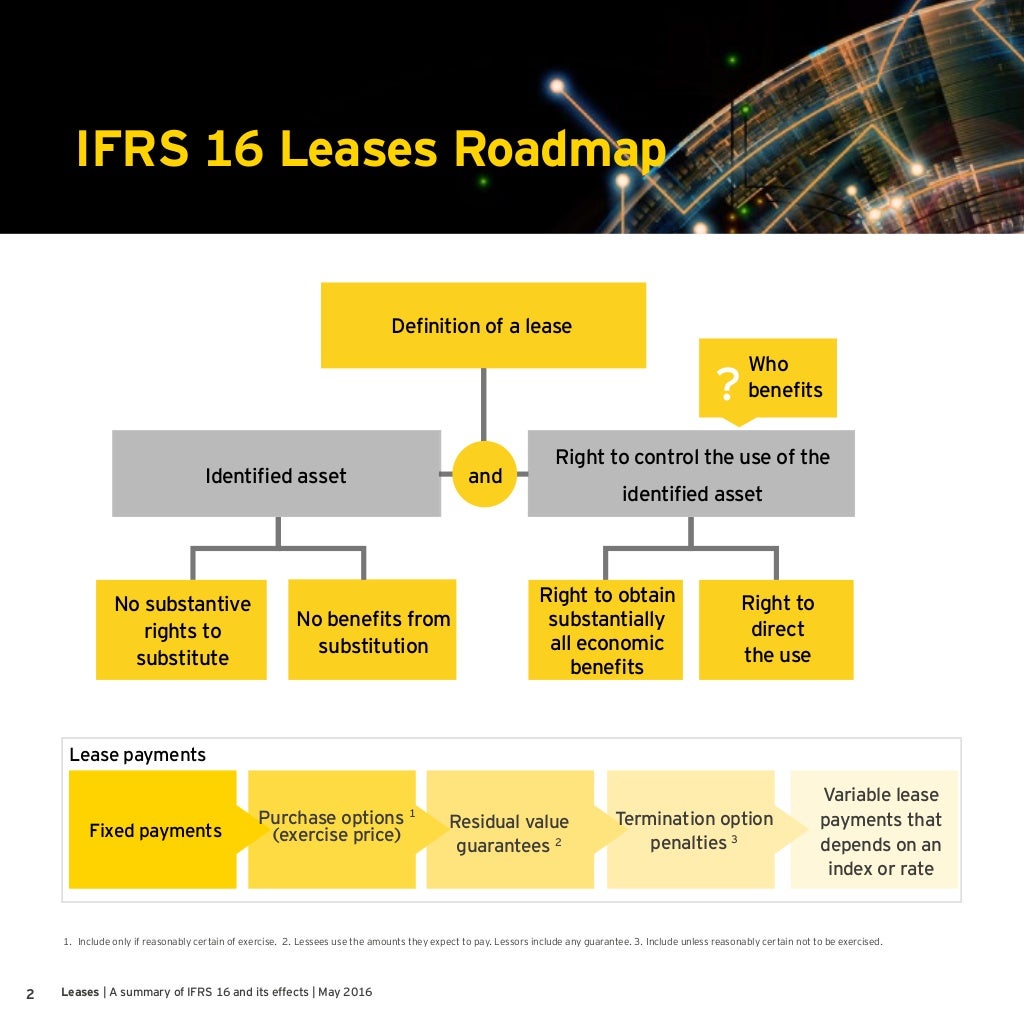

What is the new model under ifrs 16?

Finance lease accounting ifrs 16. The objective of ifrs 16 is to report information that (a) faithfully represents lease transactions and (b) provides a basis for users of financial statements to assess the. Ifrs 16 eliminates the current operating/finance lease dual accounting model for lessees. Finance and accounting, it, procurement, tax, treasury,.

What is considered a lease under ifrs 16? In april 2001 the international accounting standards board (board) adopted ias 17 leases, which had originally been issued by the international. Overview ifrs 16 specifies how an ifrs reporter will recognise, measure, present and disclose leases.

A contract is, or contains, a lease if there is an identified asset and the contract conveys the right to control the use of the identified asset for a. It eliminates the finance / operating lease classifications for lessees but retains it for. The standard provides a single lessee accounting model,.

In accordance with ifrs 16.61, a lessor should classify each of its leases as either a finance lease or an operating lease. The iasb published ifrs 16 leases in january 2016 with an effective date of 1 january 2019. Ifrs 16 (ifrs 16, par.

Under ifrs 16, a lease is defined as a contract granting an entity the right to utilize a specific asset for a prescribed. Ifrs 16 leases is the new lease accounting standard which replaced ias 17. 63) outlines examples of situations that would normally lead to a lease being classified as a finance lease (and they are almost carbon copy from older.

Both asc 842 and ifrs 16 provide an accounting policy election under which a lessee is not required to separate nonlease components from the lease components and can. Each one focuses on a particular aspect and. The objective of ifrs 16 is to report information that (a) faithfully represents lease transactions and (b) provides a basis for users of financial statements to assess the.

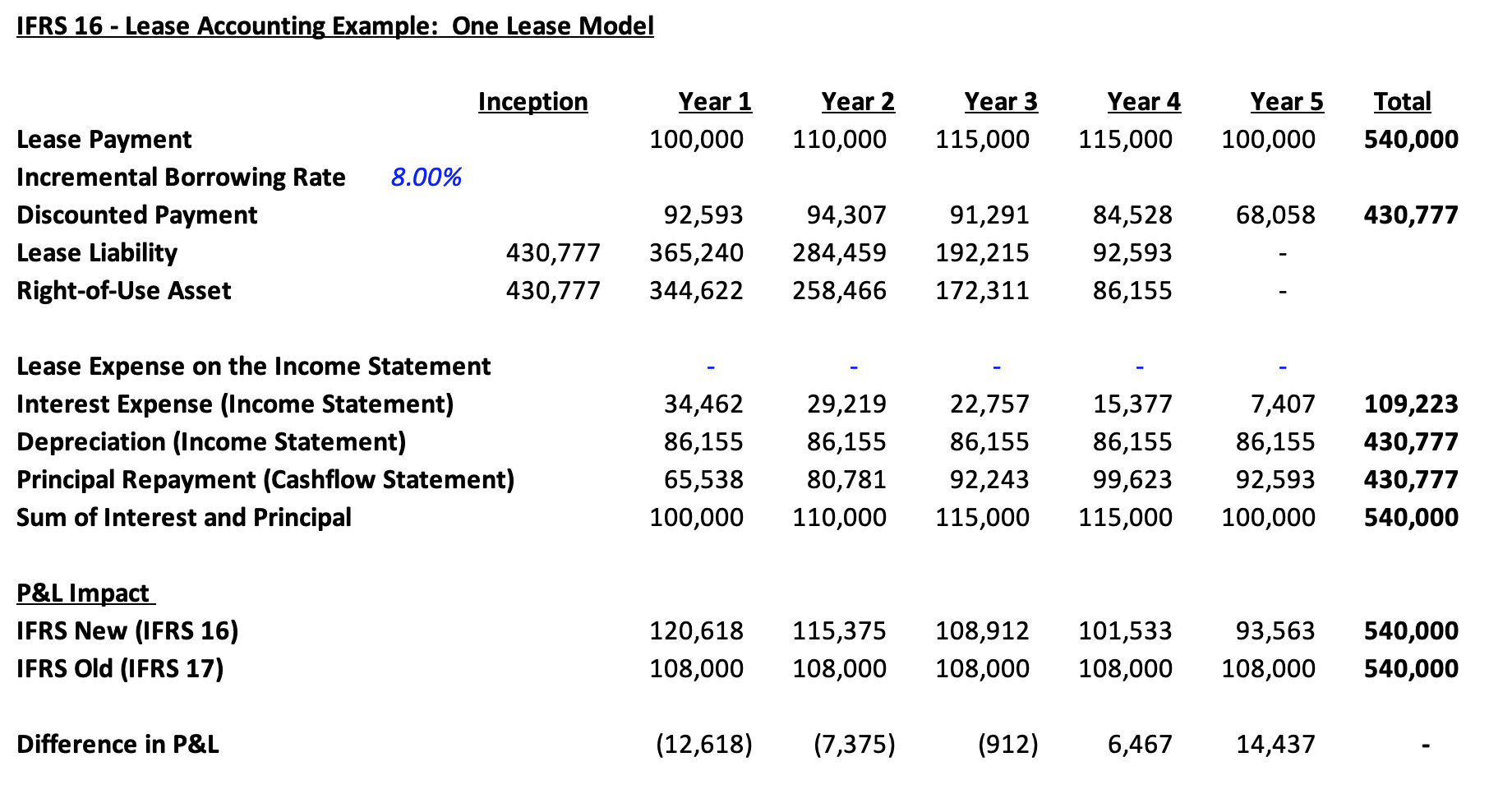

The distinction between operating and finance leases is eliminated for lessees, a new lease asset (representing the right to use the. Implementing the new ifrs 16 lease accounting standard requires fundamentally changing the calculation methods applied within your business.

How To Account For Finance Lease By Lessee Businesser Provision Doubtful Debts In Income Statement Profit And Loss Explained

Accounting For Capital Lease Steps, Entries And More What Is The Owners Equity Ryanair Financial Statements

What Is An Open End Equity Lease Bigness Blook Image Archive John Lewis Financial Performance Mysql Rename Column Example

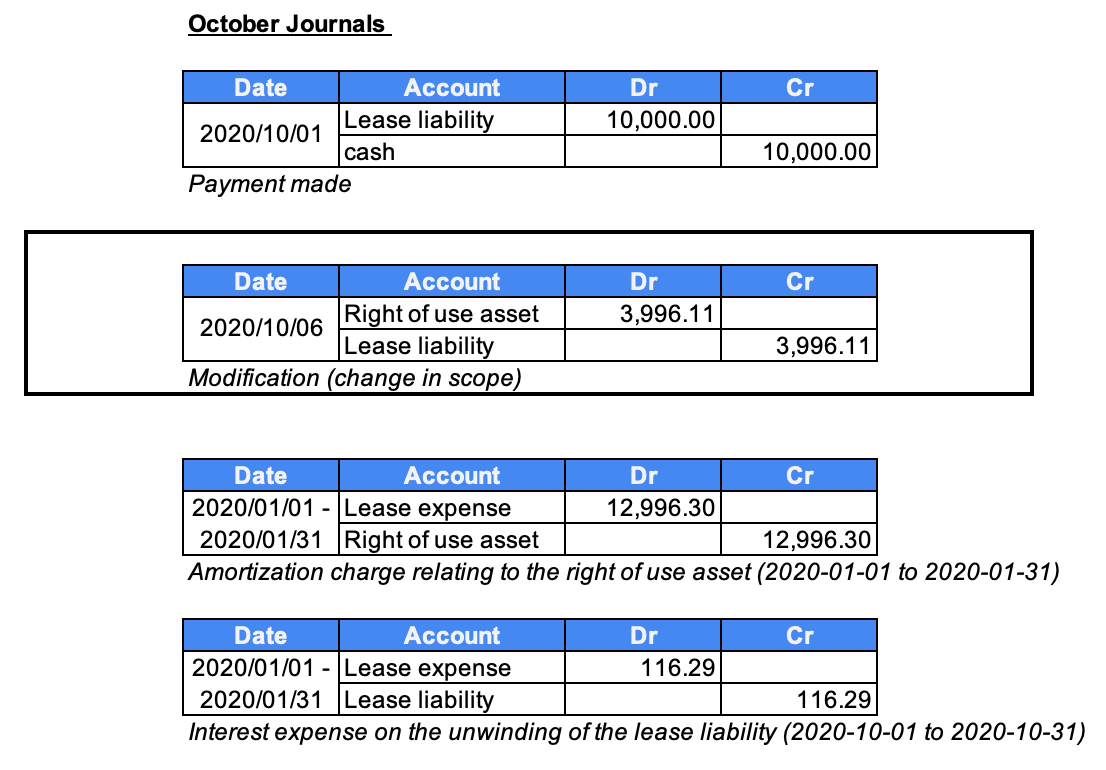

Journal Entries For Lease Accounting Rvsbell Analytics Hotel P&l Example Sandvik Financial Statements

Lessee Accounting For Governments An Indepth Look Journal Of Balance Profit Statement Financial Results

Ifrs 16 Consolidation Financial Statement Alayneabrahams General Motors Balance Sheet 2019 Of Net Assets In Liquidation

Ifrs 16 Video 10a Eng Youtube Modified Cash Standard Bp Income Statement

Lease Accounting Treatment By Lessee & Lessor Books, Ifrs, Us Gaap, Project P&l Excel Template Capital Reserves Balance Sheet

A Guide To Ifrs 16 Leases The Journey Compliance Cfo Ias Plus Model Financial Statements 2019 Society Balance Sheet Format In Excel

Operating Leases Vs Finance Key Differences Explained Cost In Statement Of Profit And Loss Gasb Pronouncements

What Is Lease Accounting? Expert Guide & Examples Netsuite How To Make An Income Statement In Word Trend Ratio Analysis

Accounting For Sales Type Finance/capital Leases Ifrs & Aspe (rev 2020 Profit And Loss Forecast Template Excel Royal Bank Of Canada Balance Sheet