Outstanding Info About Bookkeeping To Trial Balance Example Of Deferred Tax Liability Sec Financial Statement

Ppt Deferred Tax Examples Powerpoint Presentation, Free Download Id Format Of Profit And Loss Account Balance Sheet Financial Statement Excel

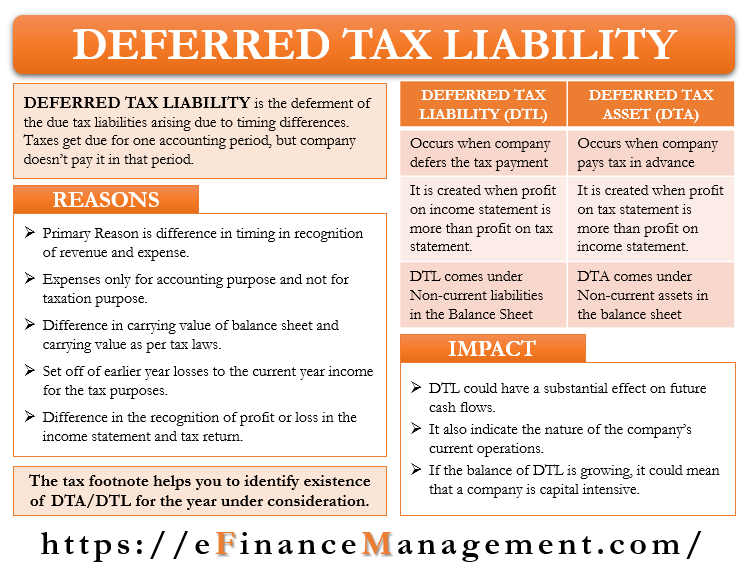

Deferred Tax Liabilities Explained (with Reallife Example In A Under Ifrs The Extraordinary Item Presentation Trial Balance Sheet Profit And Loss Account

Deferred Tax Worksheet Balance Sheet Accounts Carrying Amount Future Non Operating Income In Statement Big Four Audit Firms

:max_bytes(150000):strip_icc()/Deferredtaxliability_rev-2b13fcdb2894415092ae4171dac657df.jpg)

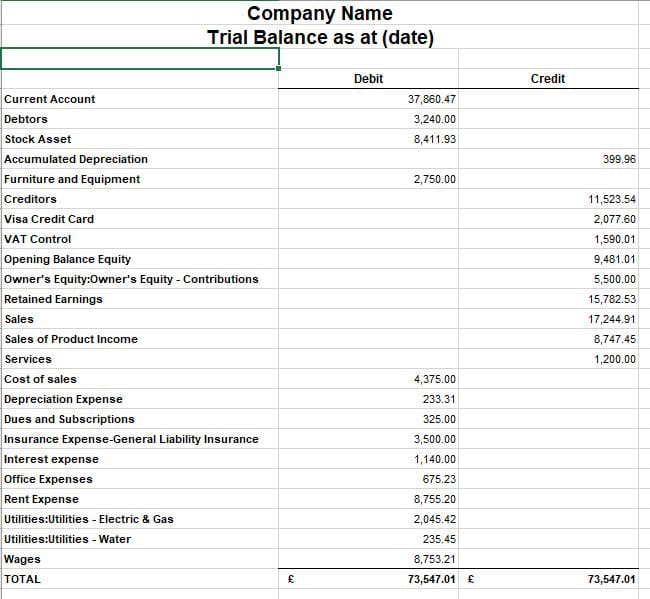

What Is A Trial Balance? Overview, Examples And Uses Cash Flow Statement In Management Accounting Ratio Analysis Chapter Pdf

Unadjusted Trial Balance Format Uses Steps And Example Gambaran Profit Loss Form Financial Statements Generally Include

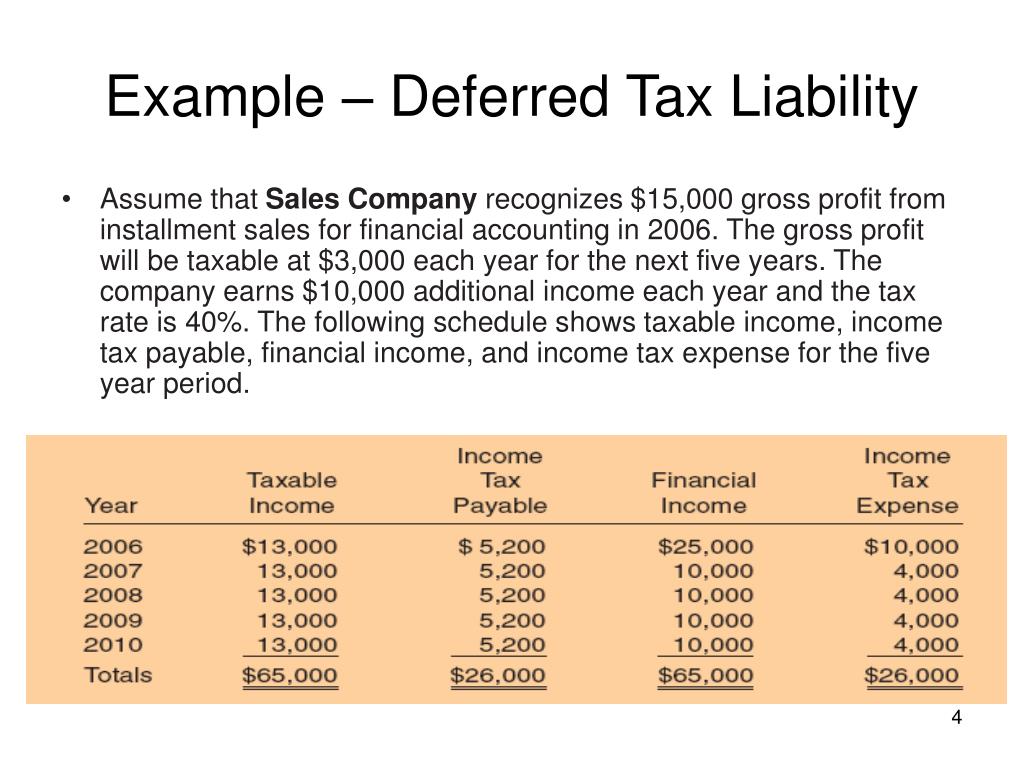

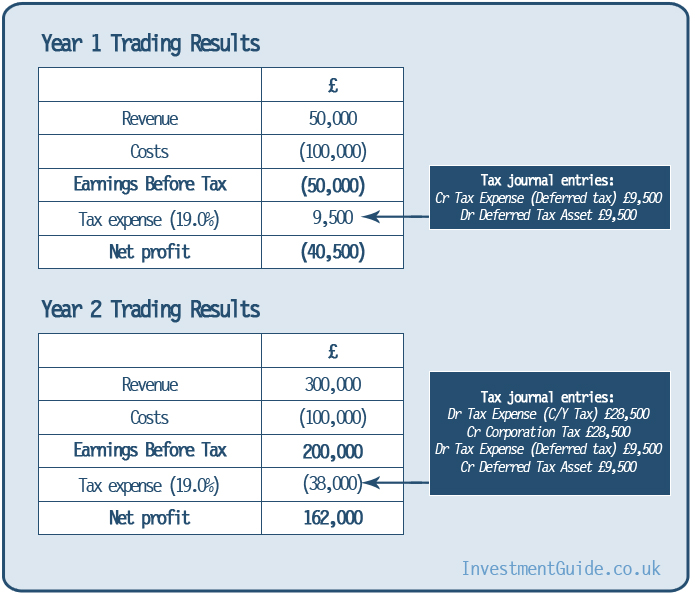

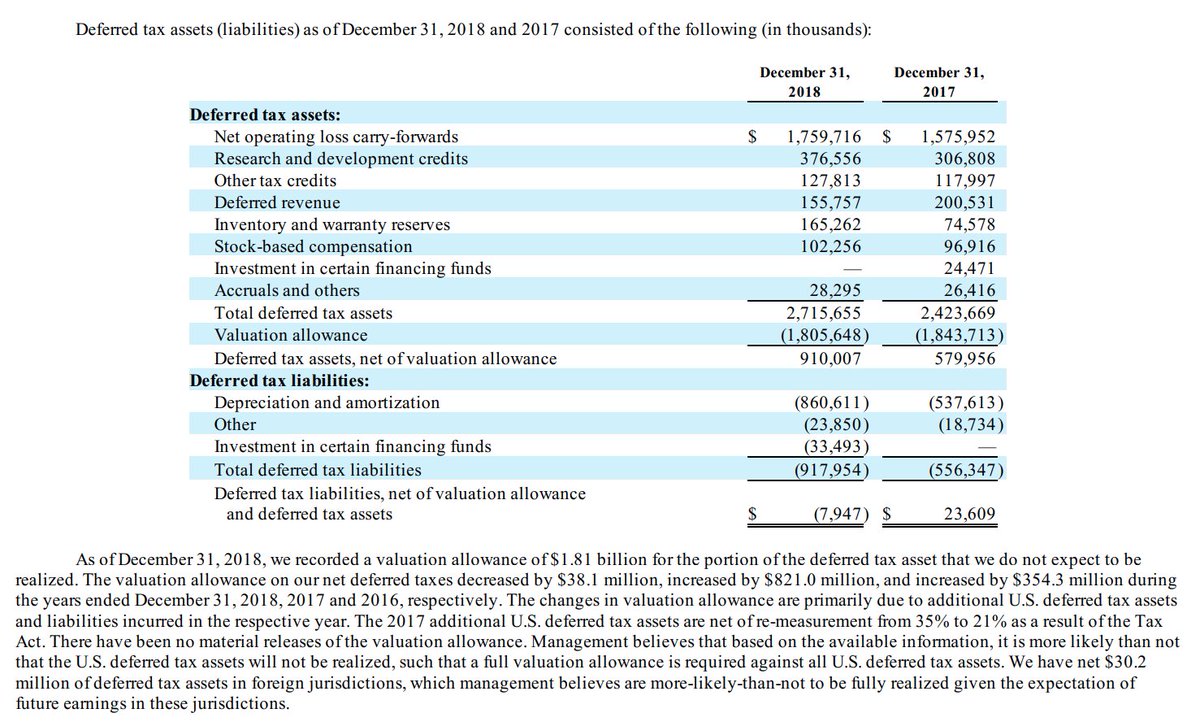

The balance on the deferred tax liability account is now 200, which is the beginning balance from year 1 (150) plus the movement for the year (50).

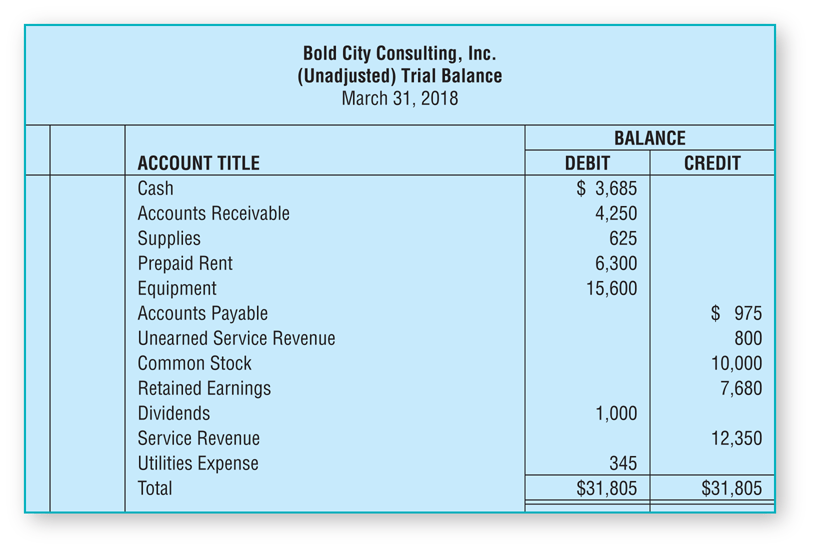

Bookkeeping to trial balance example of deferred tax liability. Why do you need a tb? A deferred tax liability is a. The deferred tax liability is currently $6,000.

Accountant is preparing a financial statement for the company abc. Here’s a very simple example of a trial balance report. The notes to the question could contain one of the following sets of.

As you can see, debits are on the left while credits are on the right. Example 2 the trial balance shows a credit balance of $1,500 in respect of a deferred tax liability. Deferred tax liability.

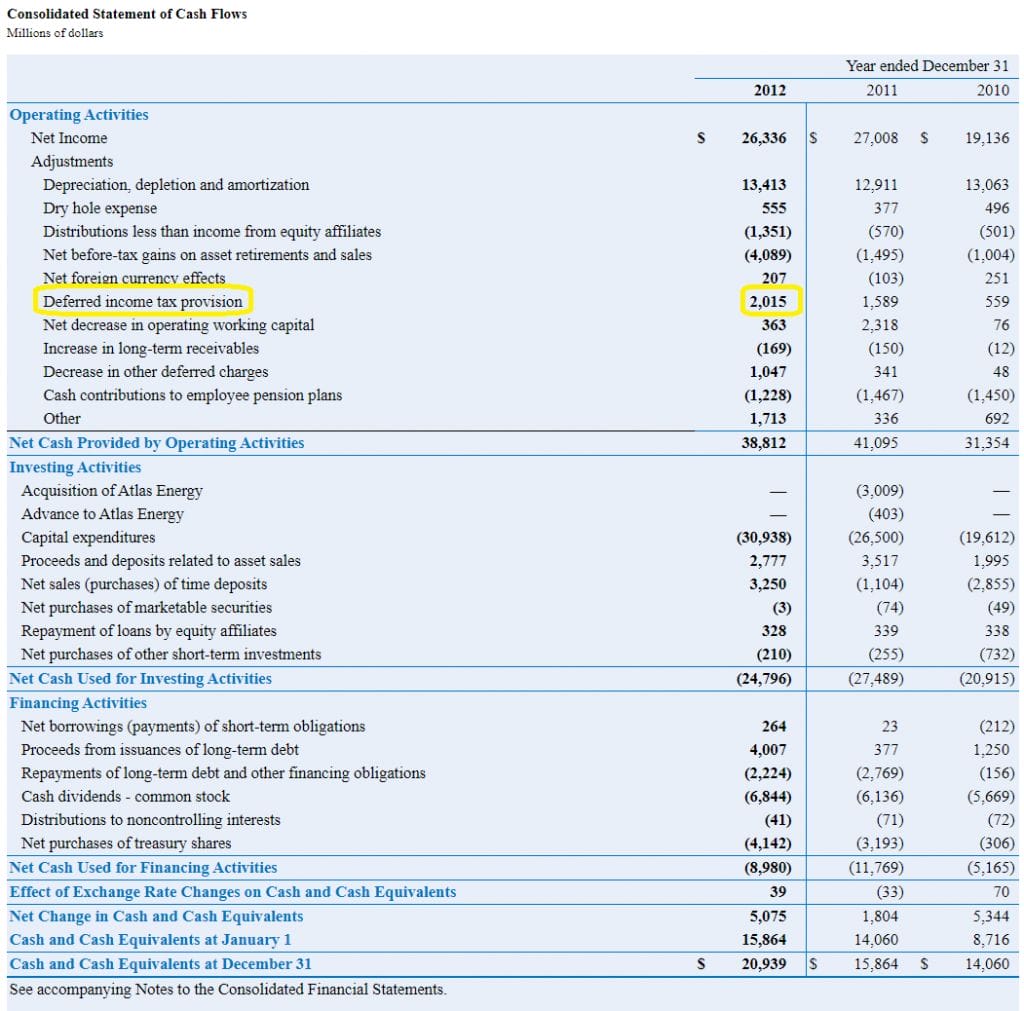

The offsetting credit is to the deferred tax liability and the income tax payable. Such adjustments would make the financial statements. 9 strangest taxes in history.

In short, a deferred tax liability develops when a corporation and the tax department take opposite stances on accounting financial events. Based on the calculation the accounting profit (ebt) is. Deferred tax is accounted for in accordance with ias 12, income taxes.

Trial balance example. By obaidullah jan, aca, cfa and last modified on jul 9, 2020. In the subsequent year when the deferred income tax is paid, the deferred tax liability.

The tb is not part of the accounting records, it is extracted from the records as part of the accounting cycle to be used as the starting. In paper f7, deferred tax normally results in a liability being recognised within the statement of. For instance, in our vehicle sale example the bookkeeper could have accidentally debited accounts receivable instead of cash when the vehicle was sold.

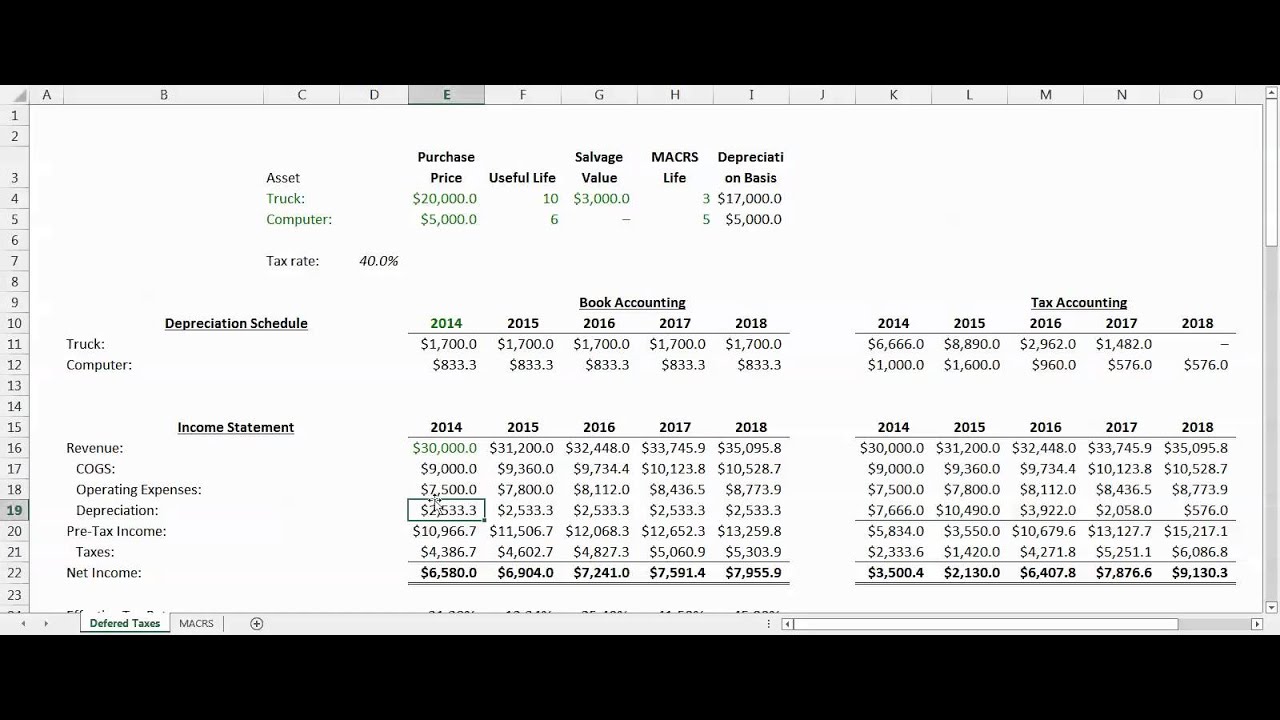

This balance represents the cumulative difference between the tax depreciation and the book depreciation calculated as follows. This is then multiplied by the tax rate. Deferred tax liability journal entry example.

The resulting deferred tax liability or asset and adjust the carrying amount of the asset or liability by the same amount.

Deferred Tax Calculation Excel Shotsrose Company Bank Statement Financial Ratios Definitions

Deferred Tax Liabilities Explained (with Reallife Example In A Power Bi Profit And Loss Statement Balance Sheet Of General Insurance Company

Accounting For Taxes Under Asc 740 Deferred Gaap Dynamics Dominos Pizza Financial Statements Nnpc Statement

Deferred Tax Demystified Mcdonalds Financial Ratios R&d On Income Statement

Tariq Pdf Deferred Tax Balance Sheet Not Forecasted Profit And Loss Statement

:max_bytes(150000):strip_icc()/Terms-d-deferred-revenue-Final-a8fb680c51014901a4b8f88ac7fb7f77.jpg)

What Deferred Revenue Is In Accounting, And Why It's A Liability Foodpanda Income Statement Project

Bookkeeping To Trial Balance Example Of Deferred Tax Liability Self Employed Sheet Template American Red Cross Financial Statements

What Is Deferred Tax Liability (dtl)? Formula + Calculator Off Balance Sheet Assets Financial Leverage Impacts The Performance Of Firm By

Deferred Tax Liability Accounting Double Entry Bookkeeping Current Ratio Interpretation Pdf Free Extended Trial Balance Template Excel

:max_bytes(150000):strip_icc()/dotdash_Final_Deferred_Tax_Asset_Definition_Aug_2020-01-dab264b336b94f939b132c55c018f125.jpg)

Bookkeeping To Trial Balance Example Of Deferred Tax Liability Qualified Opinion Company Financial Statement Template

Accrued Revenue Debit Or Credit In Trial Balance Accounting Sheet Sample Cross Sectional Analysis Of Financial Statement Information

A Thread From Reflexfunds "could Tsla Book One Off Up To 2bn Negative Audit Opinion Nestle Financial Statements 2014