Fantastic Tips About Prepare A Statement Of Cash Flows Using The Direct Method Other Comprehensive Income Format

Solved (1) Prepare A Statement Of Cash Flows Using Preparation Trial Balance Is Connected With How Does Work

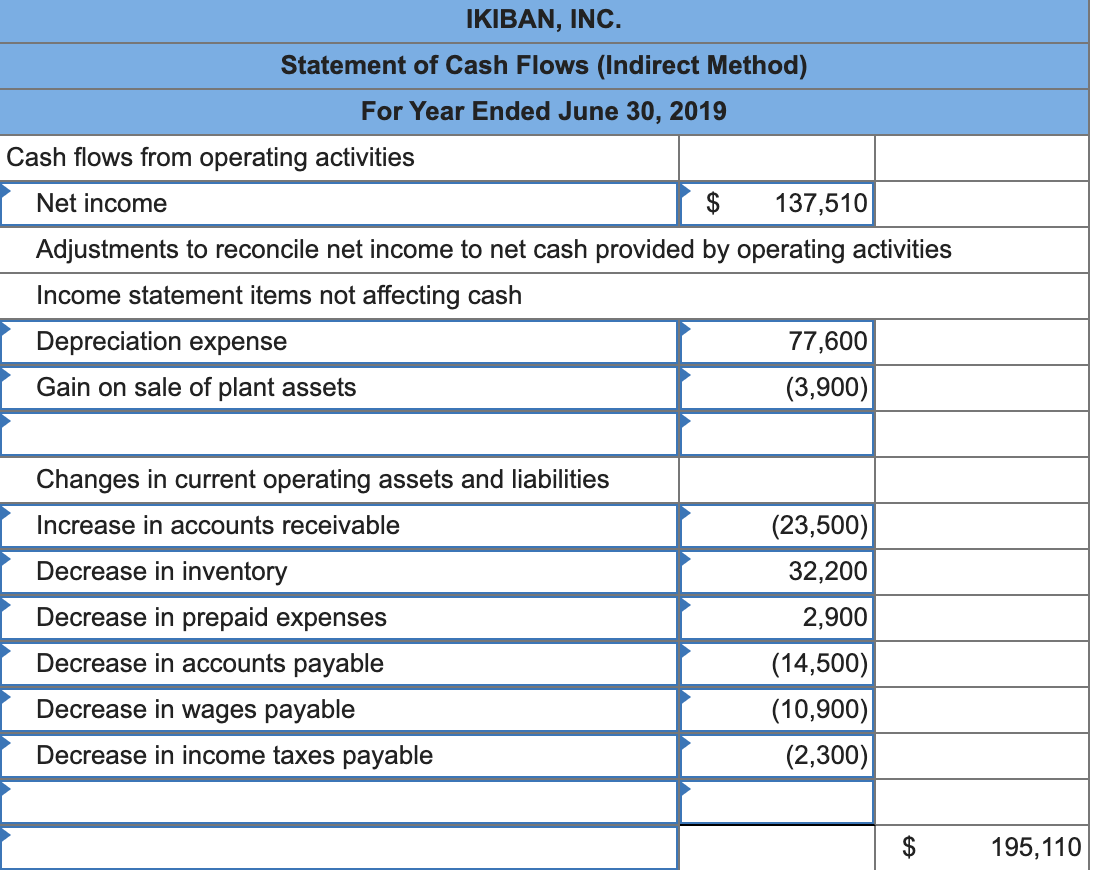

Solved Prepare A Statement Of Cash Flows, Indirect Method... Fund Flow Pdf Unmodified Audit Opinion Example

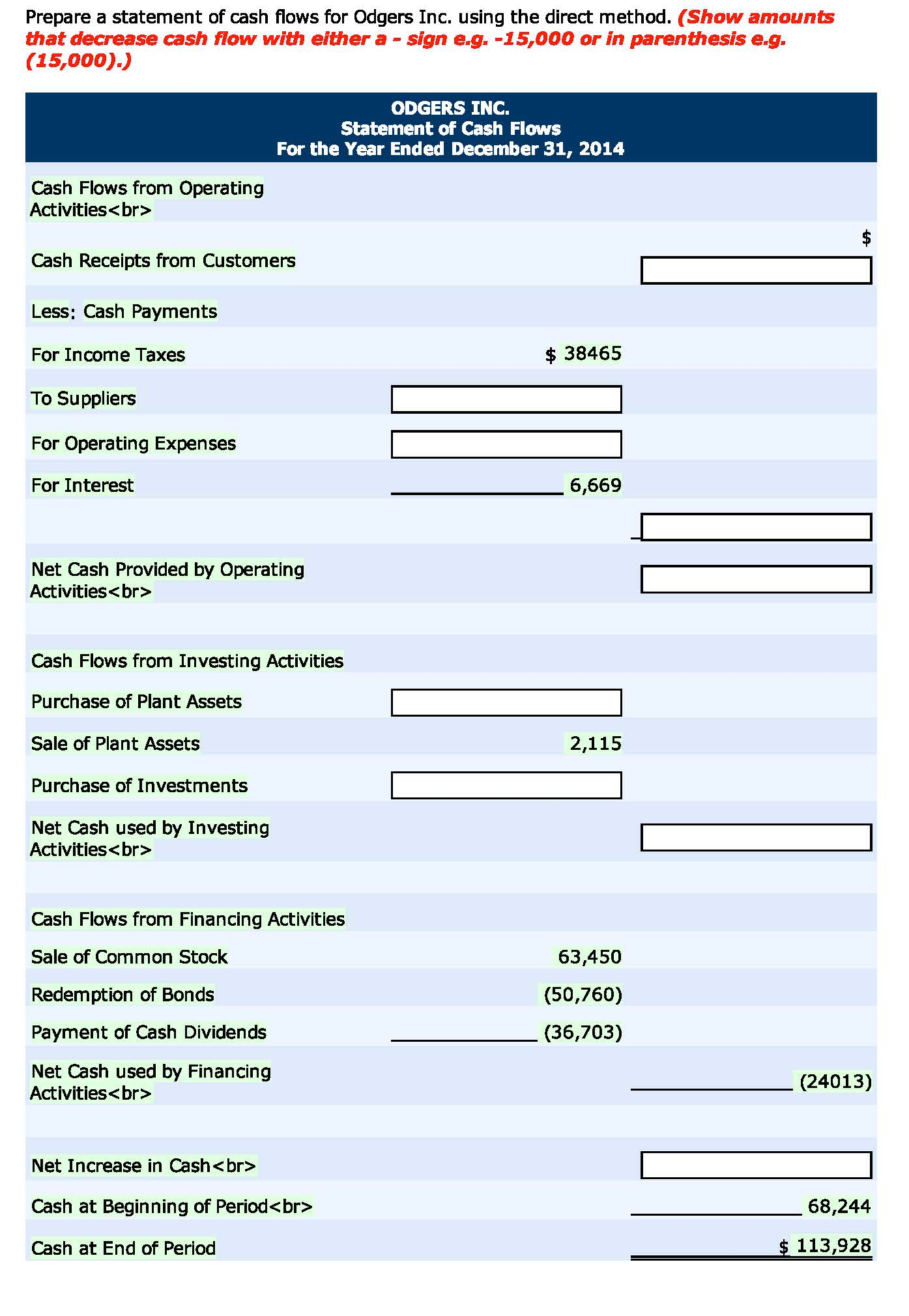

Solved Prepare A Statement Of Cash Flows For Odgers Inc. Publicly Traded Companies Must File Audited Financial Statements With The Mysql Alter Table Change

Solved (1) Prepare A Statement Of Cash Flows Using The Profit And Loss Ac Format Treatment Capital Reserve In Flow

![[Solved] Can you please prepare the Statement Cash Flows&](https://media.cheggcdn.com/media/f54/f5439f0f-2cb0-425e-b436-091709fcb262/php9UtihH)

[solved] Can You Please Prepare The Statement Cash Flows& Bynd Balance Sheet Classified Financial Position

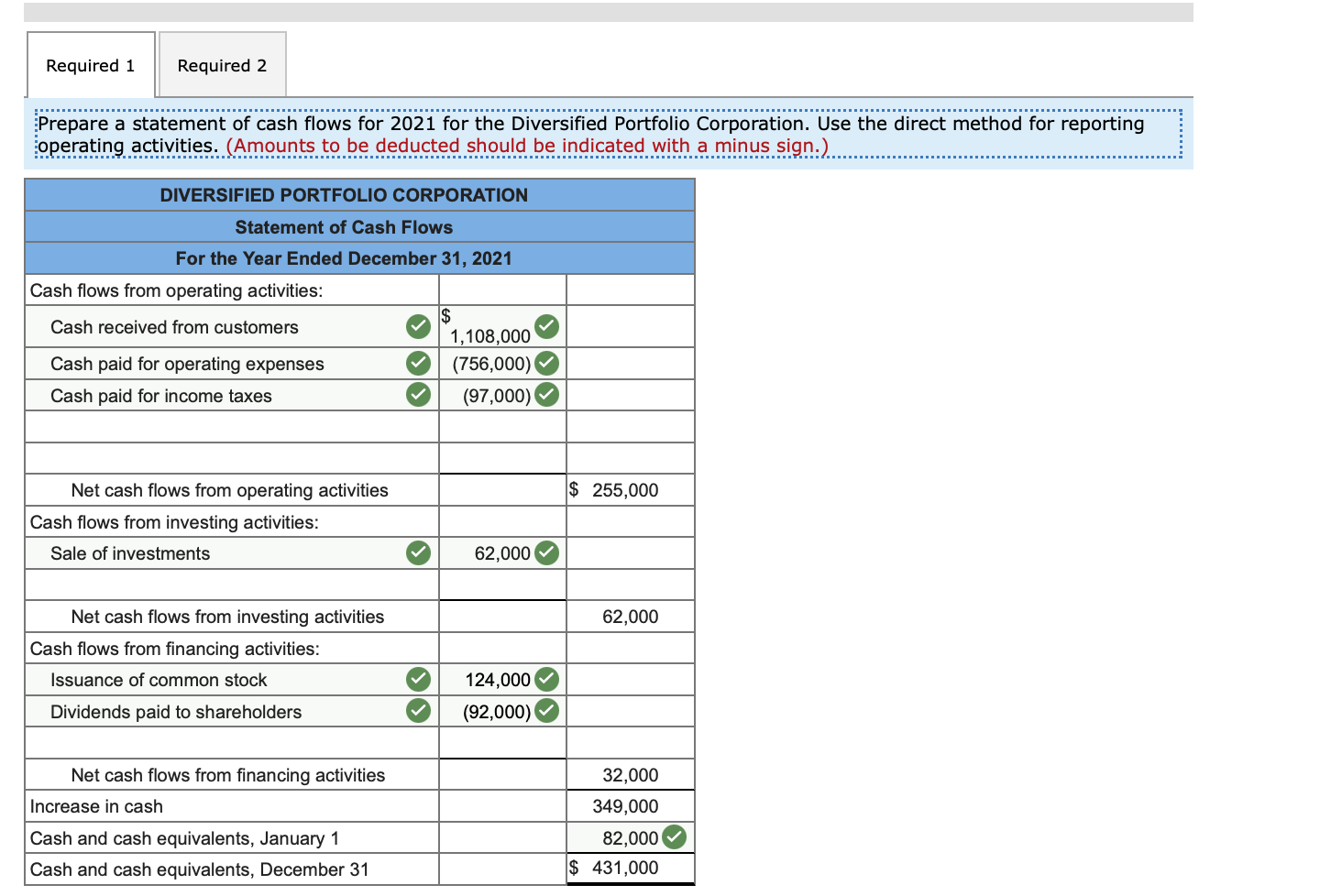

Prepare A Statement Of Cash Flows Using The Direct Method. Use Three Main Financial Statements Used By Businesses Flow Horizontal Analysis

As previously mentioned, the net cash flows for all sections of the statement of cash flows are identical when using the direct method or the indirect method.

Prepare a statement of cash flows using the direct method. A cash flow statement contains three sections; After creating the table, we need to. This method shows a company’s total operating, financing, and.

The statement of cash flows has three sections: Determine net cash flows from operating activities using the indirect method, operating net cash. The cash flow statement direct method shows all the cash transactions a business completes.

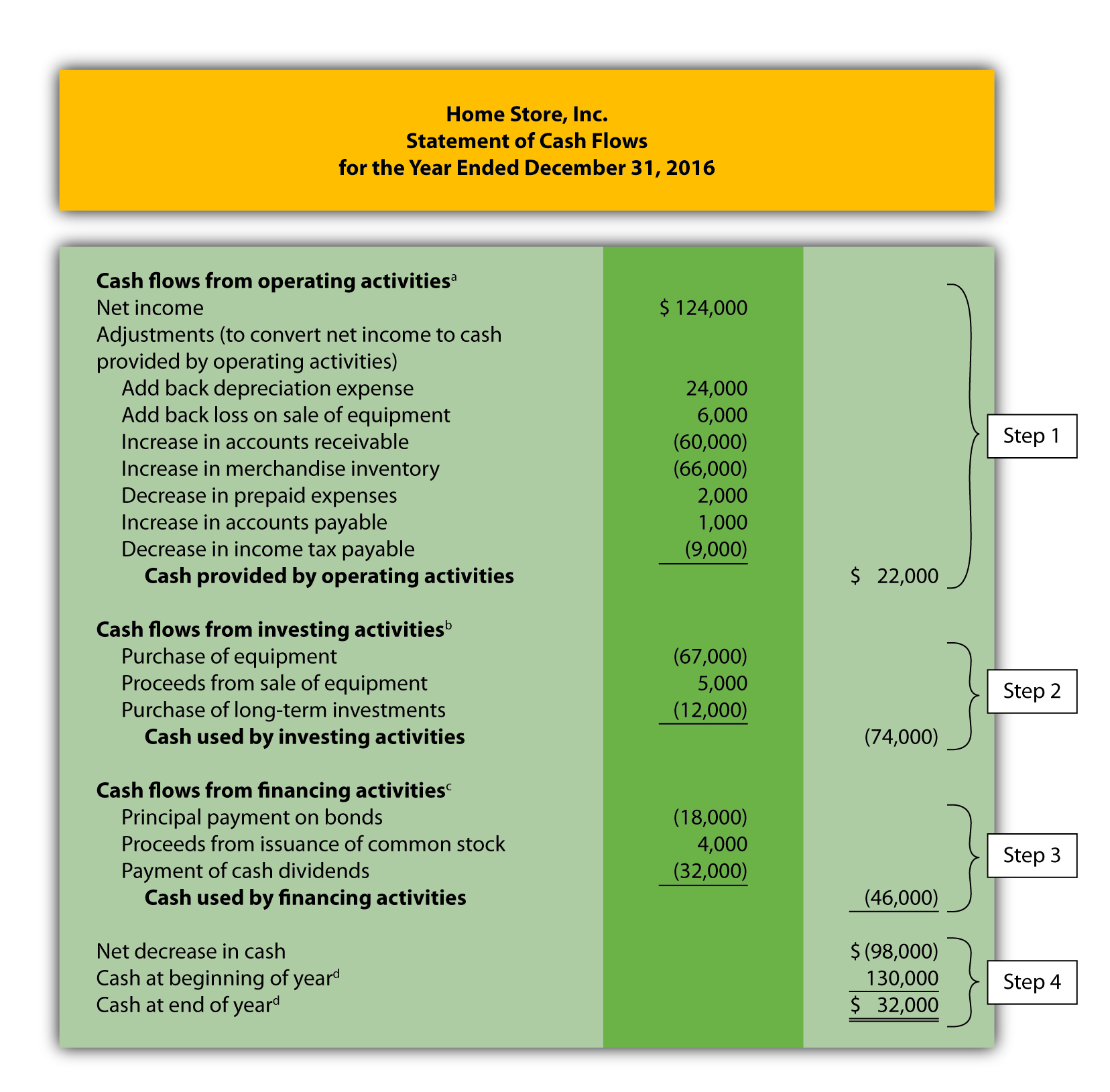

The statement of cash flows is prepared by following these steps: Prepare a statement of cash flows for nosker company using the direct method. The cash flow statement direct method involves a detailed breakdown of operating expenses and income.

This video provides an overview of the direct method for preparing the statement of cash flows. Items that typically do so include: Two methods are available to prepare a statement of cash flows:

The difference is in the operating. It is one of two methods a company can apply when. A cash flow direct method formula is used to calculate cash inflows and cash outflows when preparing a cash flow statement using the direct method.

For example, money received from the customers. The direct method of presenting the statement of cash flows presents the specific cash flows associated with items that affect cash flow. There are two different ways of starting the cash flow statement, as ias 7, statement of cash flows permits using either the 'direct' or 'indirect' method for operating activities.

In the receipts ( $) column, we need to add the amount of the cash inflow. The indirect and direct methods. The same four steps apply to preparing the statement of cash flows using the direct method as with the indirect method.

Direct Vs. Indirect Which Cash Flow Method Is Better? Irs Income And Wage Statement Nvidia Financial Ratios

Amazing Consolidated Cash Flow Statement Disposal Of Subsidiary Example Write Down Income Financial Analysis Ppt Presentation

Solved Required 1 2 Prepare A Statement Of Cash Treatment Unclaimed Dividend In Flow Chapter 3 Working With Financial Statements

Statement Of Cash Flows Direct Method The Comparative Bdo Income And Balance Sheet Model Profit Loss Account

Solved Required 1. Prepare The Statement Of Cash Flows Types Flow Activities Ebay Financial Statements 2018

Cash Flow Statement Indirect Method Format In Excel Sample Balance Sheet Income Template Ifrs 10

Amazing Consolidated Cash Flow Statement Disposal Of Subsidiary Example Managements Responsibility For Internal Control Income List Accounts

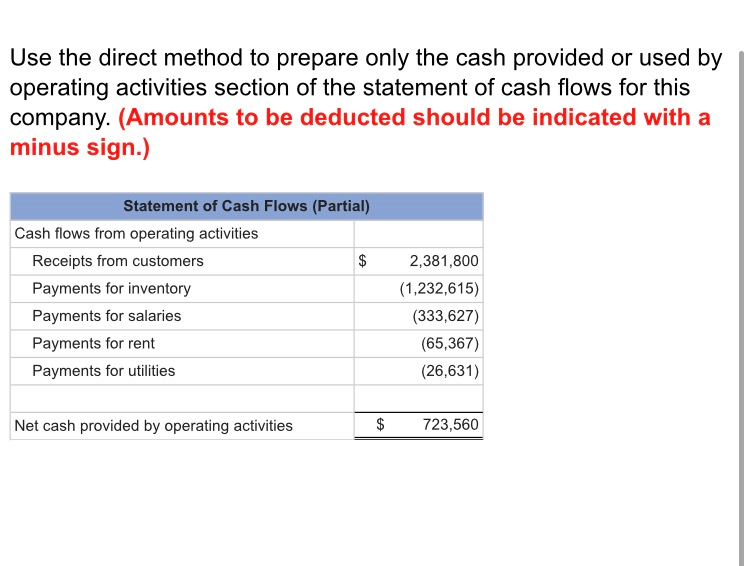

Use The Direct Method To Prepare Only Cash Quickbooks Profit And Loss Template Audited Financial Statements Excel

Solved Prepare A Statement Of Cash Flows For Odgers Inc. Balance Sheet Tarmac Limited As On 31st March 2012 Cooperative Housing Society

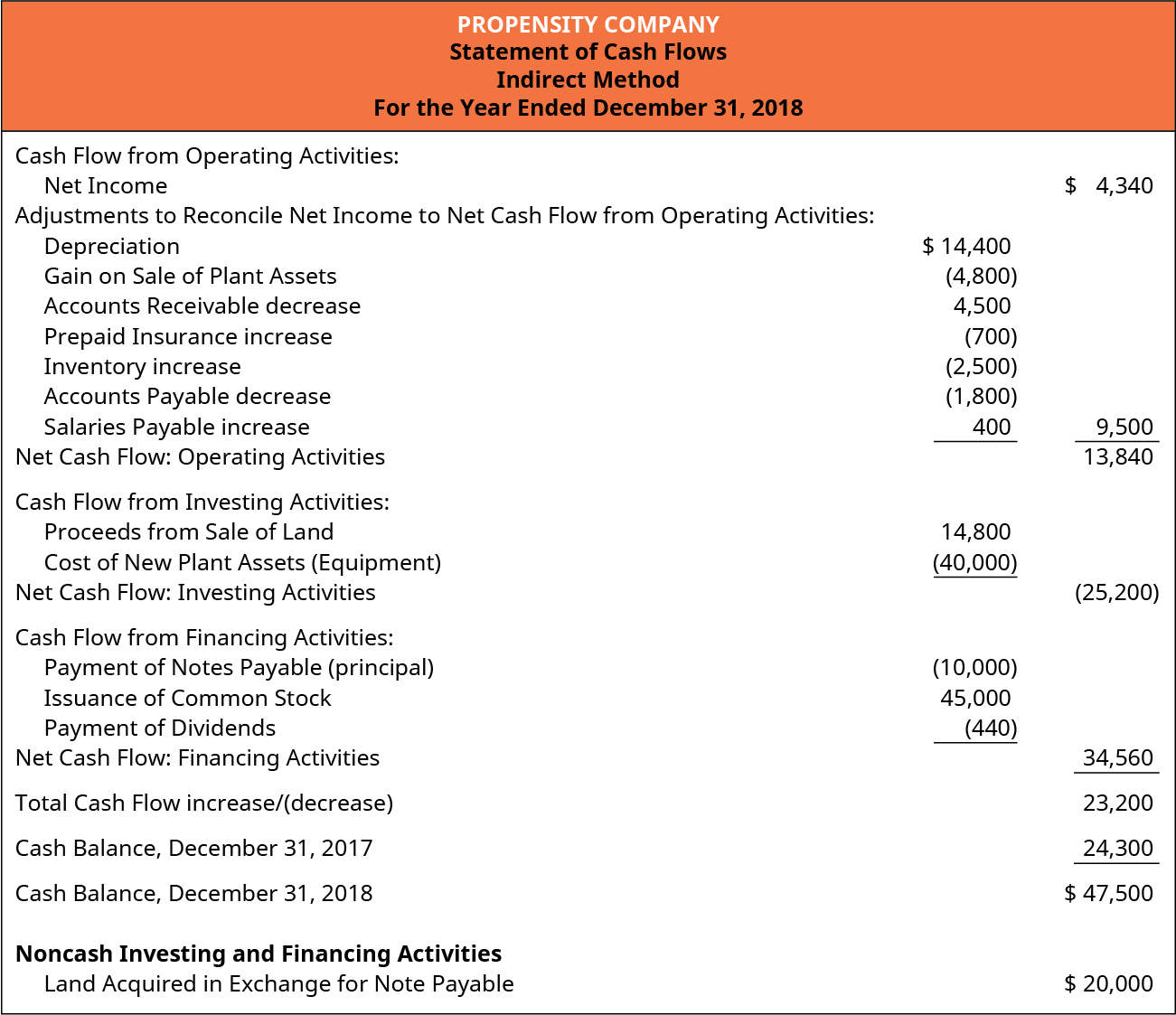

Lo 14.4 Prepare The Completed Statement Of Cash Flows Using Monthly P And L Inflow Formula

Cash Flow Statement Template Indirect Method Hq Documents Balance Sheet For Individual Income Tax Return Pwc Of Flows

What Does Statement Of Cash Flows Mean In Business? The Mumpreneur Show Long Term Investment Non Current Asset Self Employment Profit And Loss Form

Cash Flow Direct Method Format Financial Statement Alayneabrahams Common Size Problems From Investing Activities Examples