Sensational Info About Closing Entry For Retained Earnings Required Financial Statements Under Gaap

Chapter 3 Add Depreciation, Closing Entries, 4 Diff Timelines Accts, Interest Expense On Statement Of Cash Flows Profit Loss Account Template

How To Fix Closing Entry Retained Earnings In Quickbooks Jony Advertising Expense Income Statement View 26as

Closing Entries Definition, Types, And Examples Balance Sheet In Healthcare Finance Tfg Financial Statements

Elainefvmack Statement Of Accounting Standards Excel Financials

Retained Earnings Everything You Need To Know About Understanding Cash Flows Flow Analysis Of A Company

Closing Entries I Summary Accountancy Knowledge Different Types Of Financial Statements Llc Balance Sheet Example

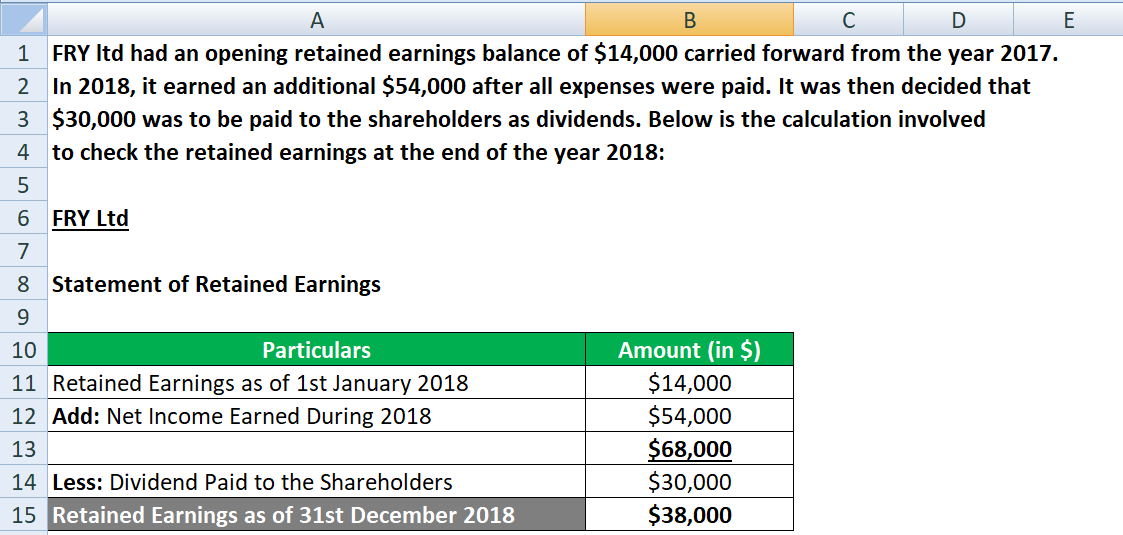

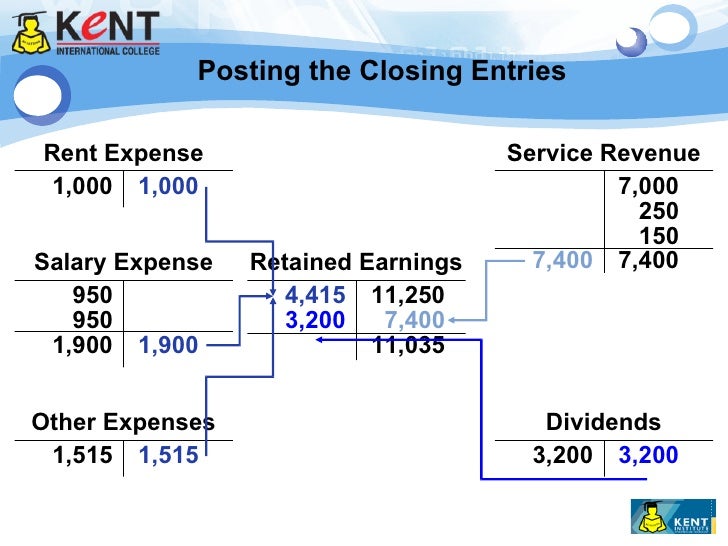

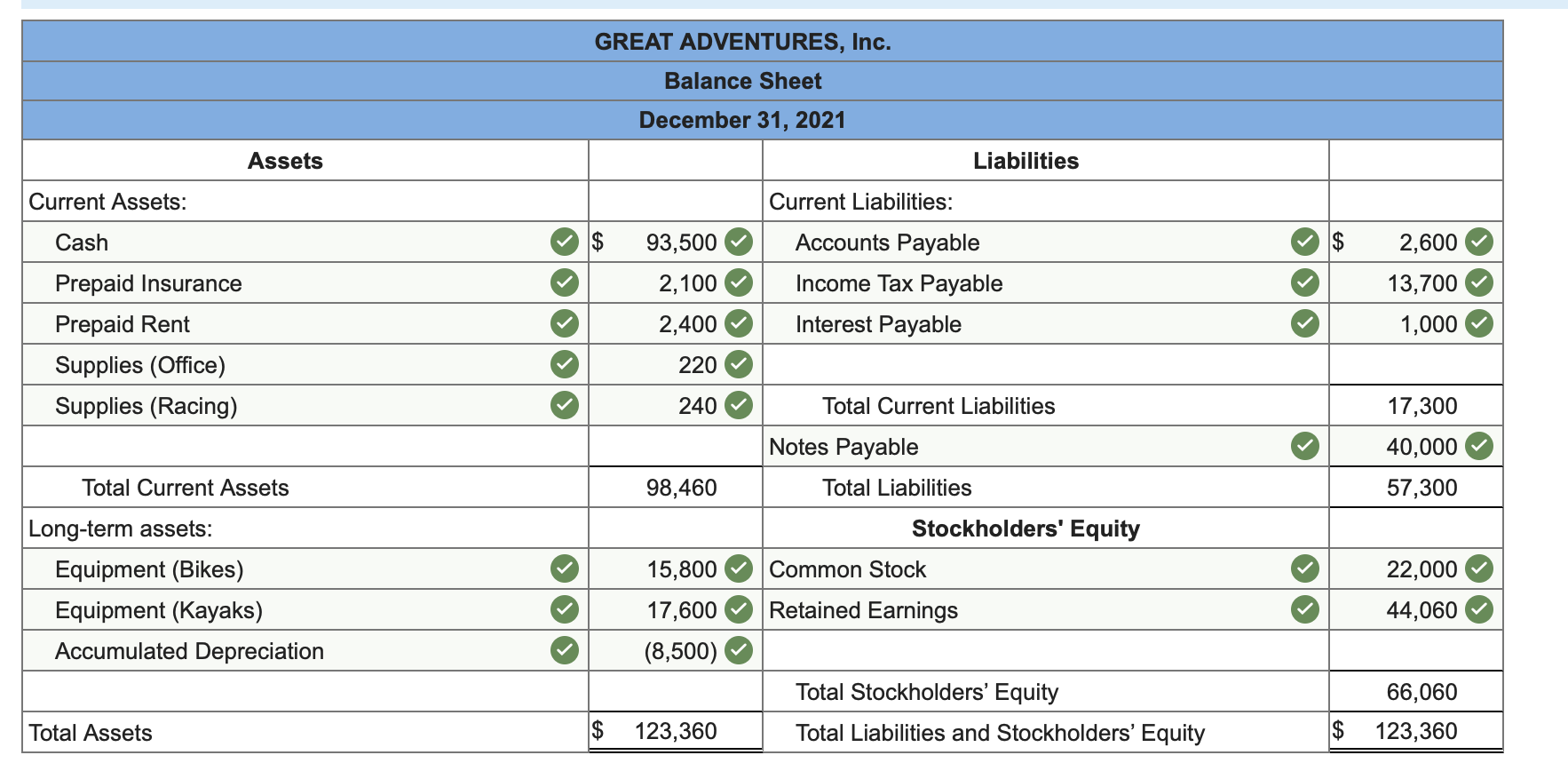

The retained earnings account is updated from the statement of change in equity accounts.

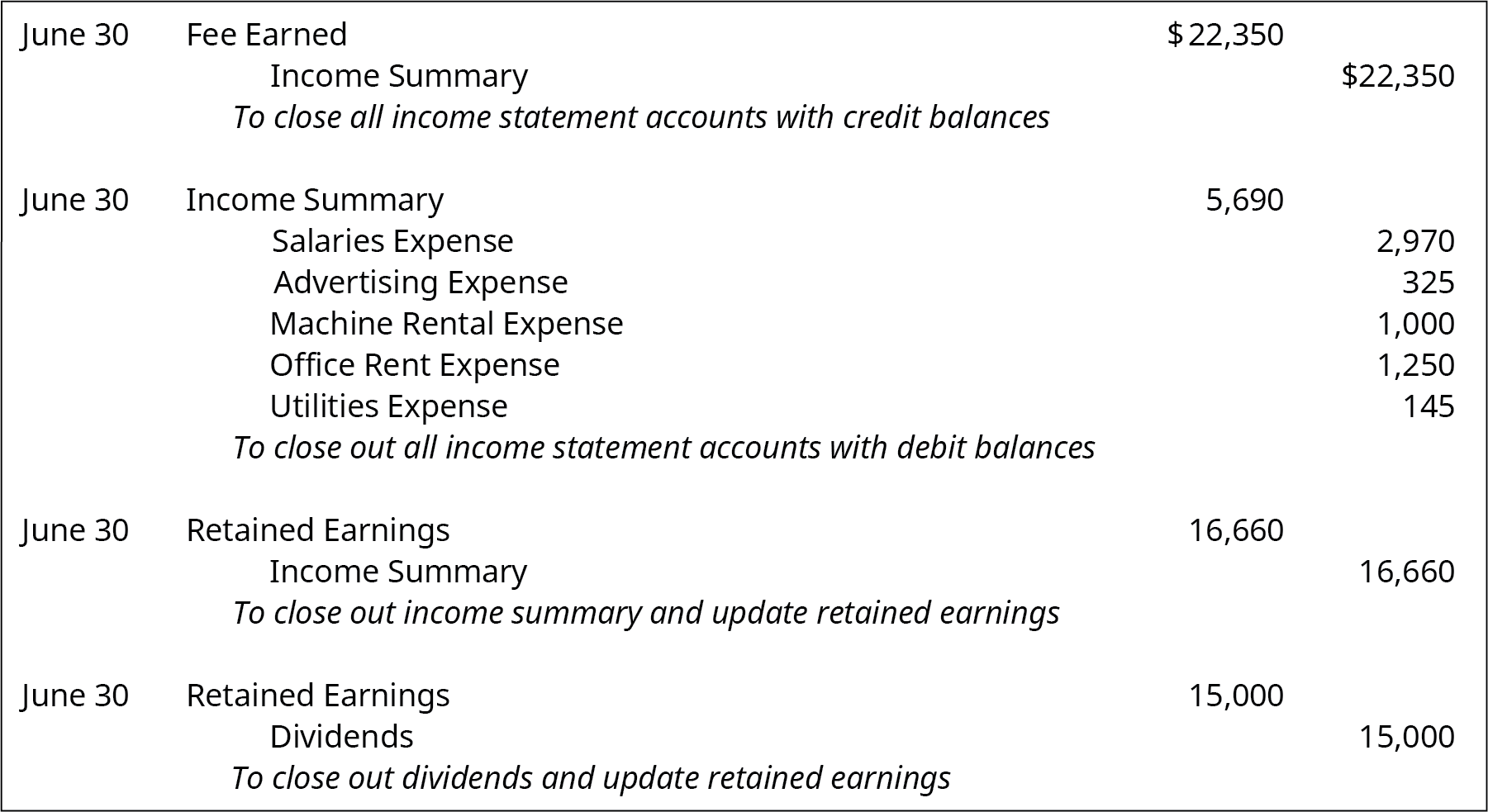

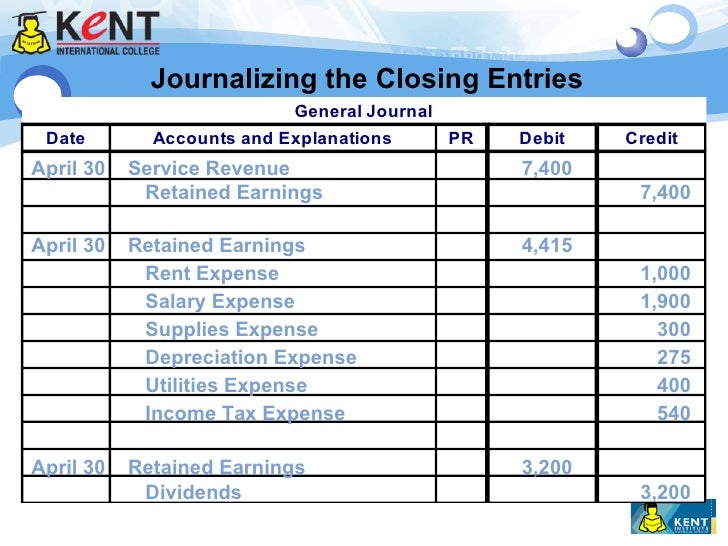

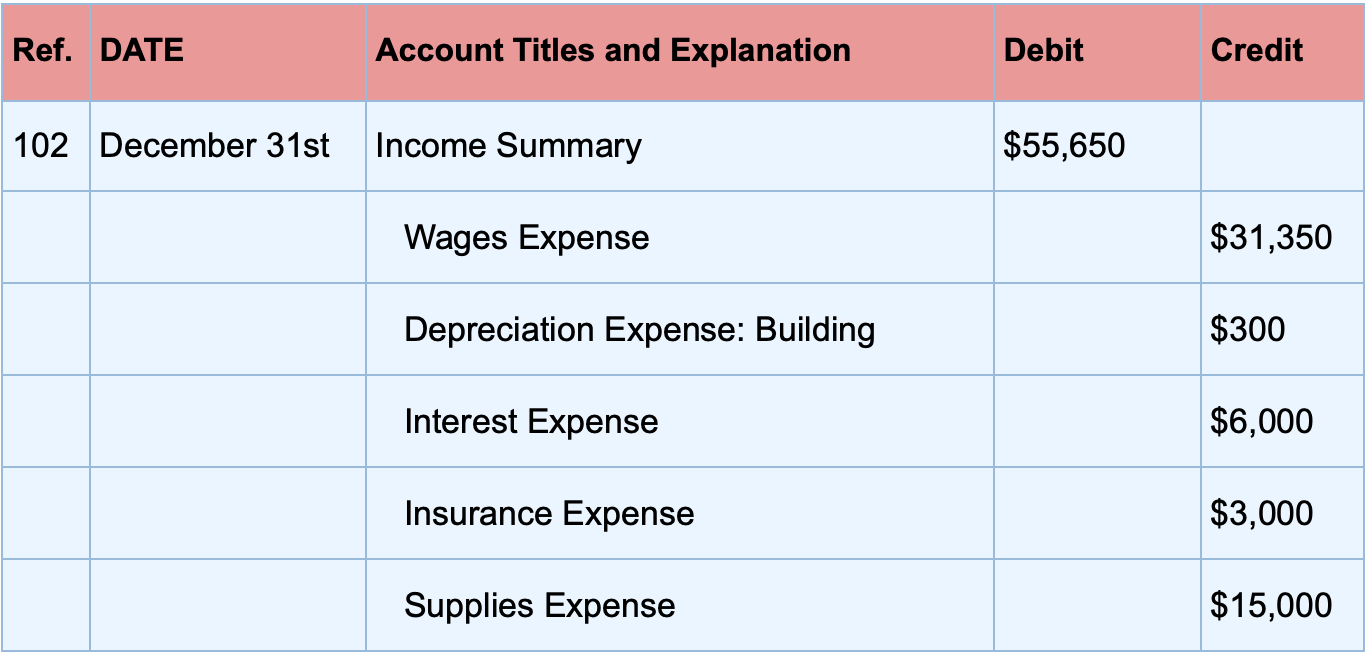

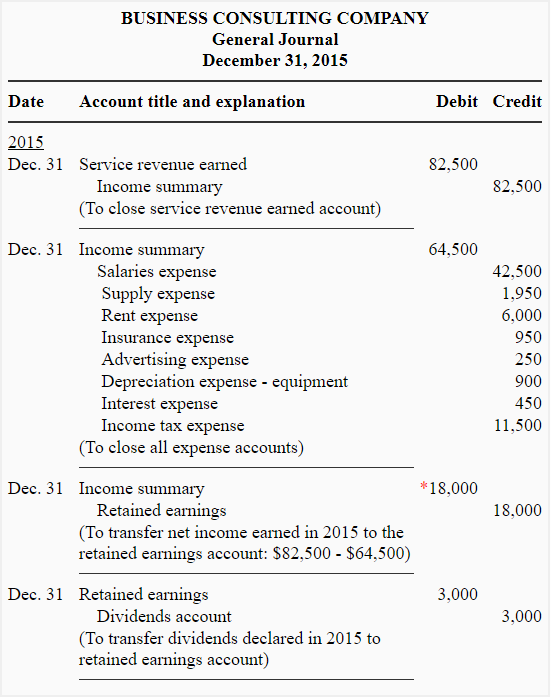

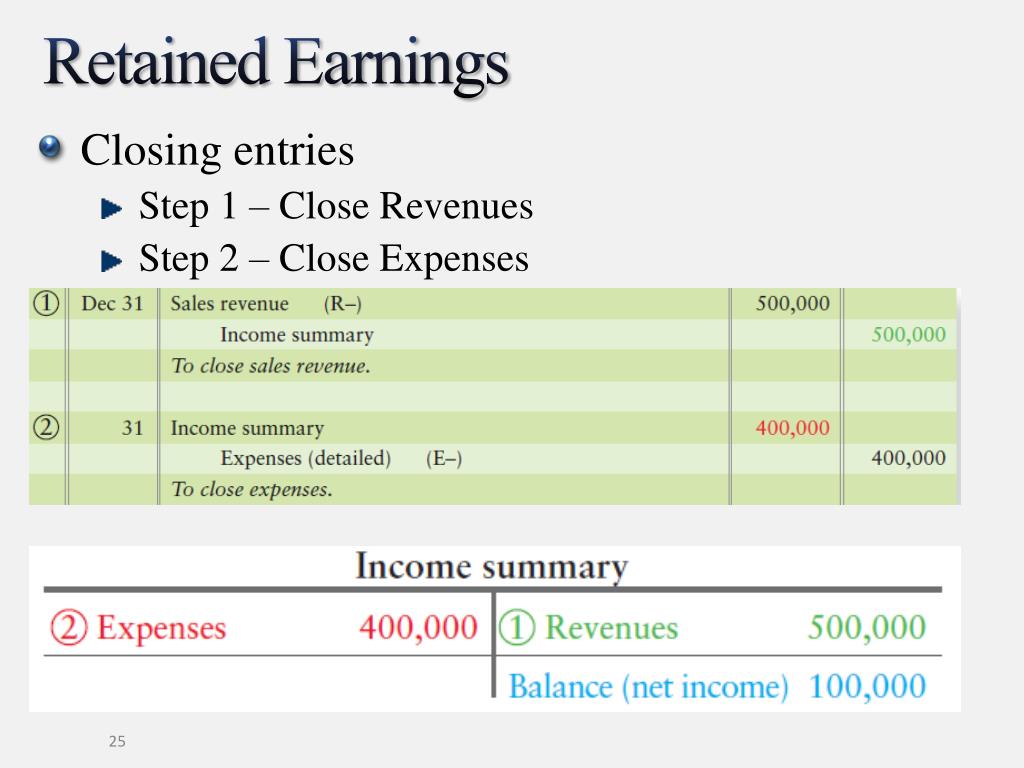

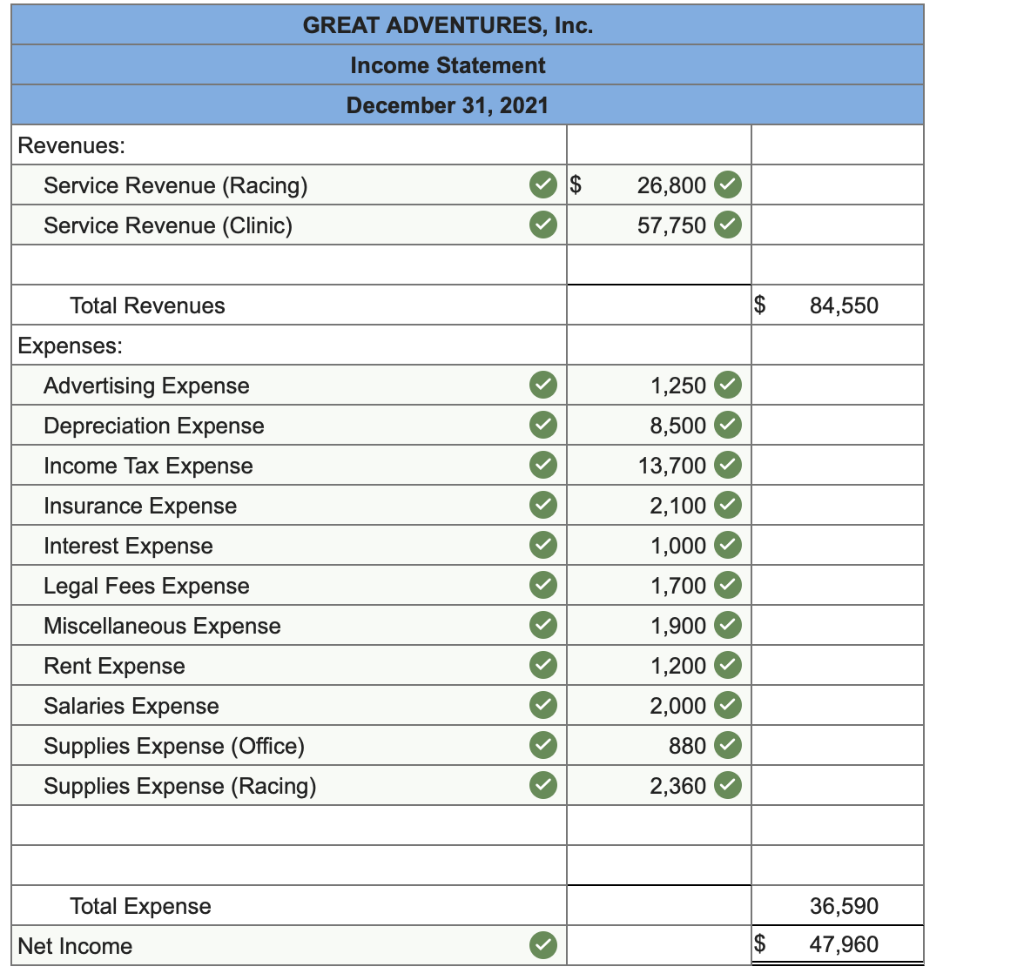

Closing entry for retained earnings. Find out the four steps, the temporary accounts, and the example of closing. The purpose of closing entries. The last entry is to close out dividends.

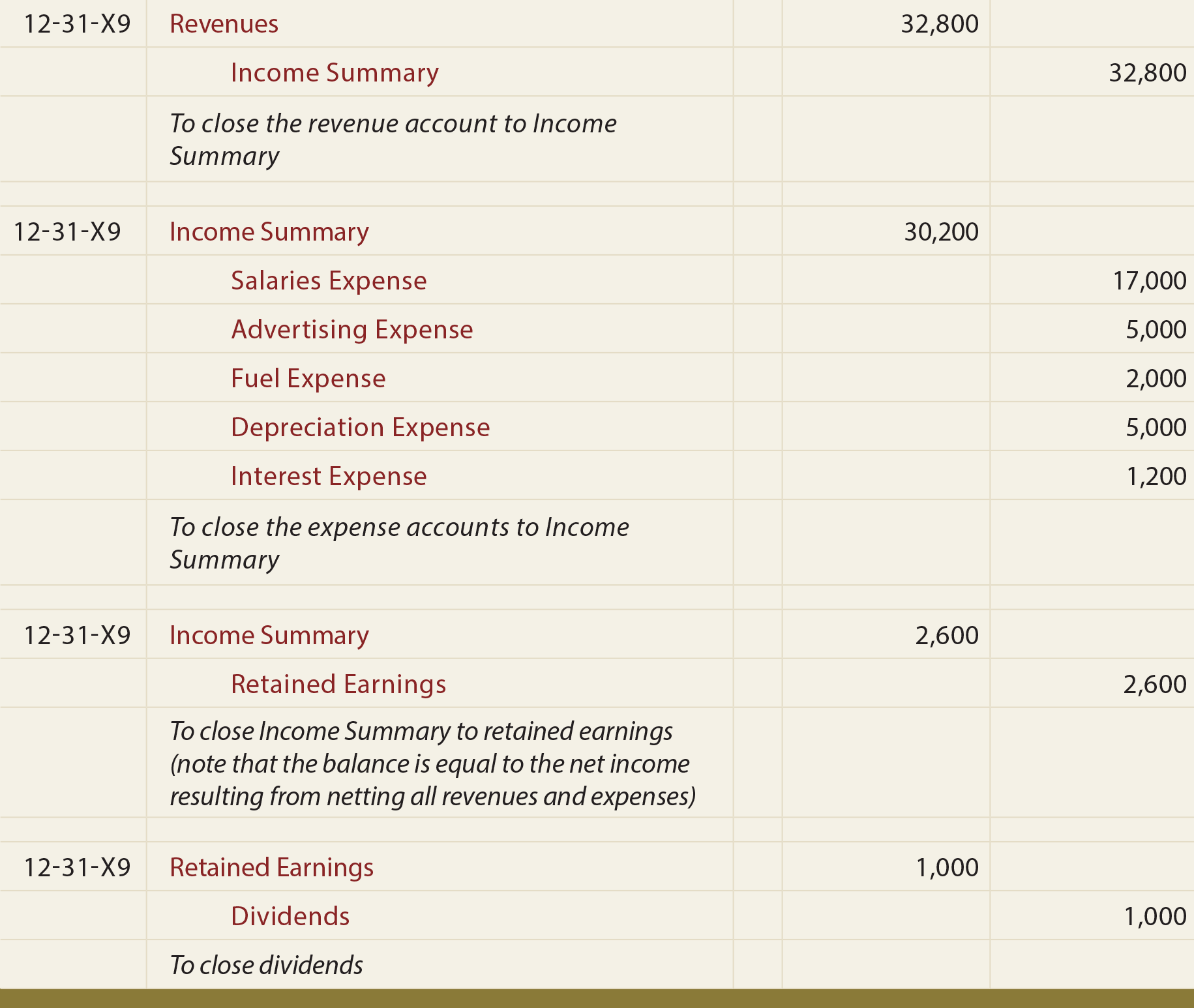

If your company doesn’t have dividends then you won’t need to do this step. Close revenue accounts clear the balance of the revenue account by debiting revenue and crediting income summary. Closing the net income to retained earnings if the company makes a profit during the year, it can make the closing entry for net income by debiting the income summary account.

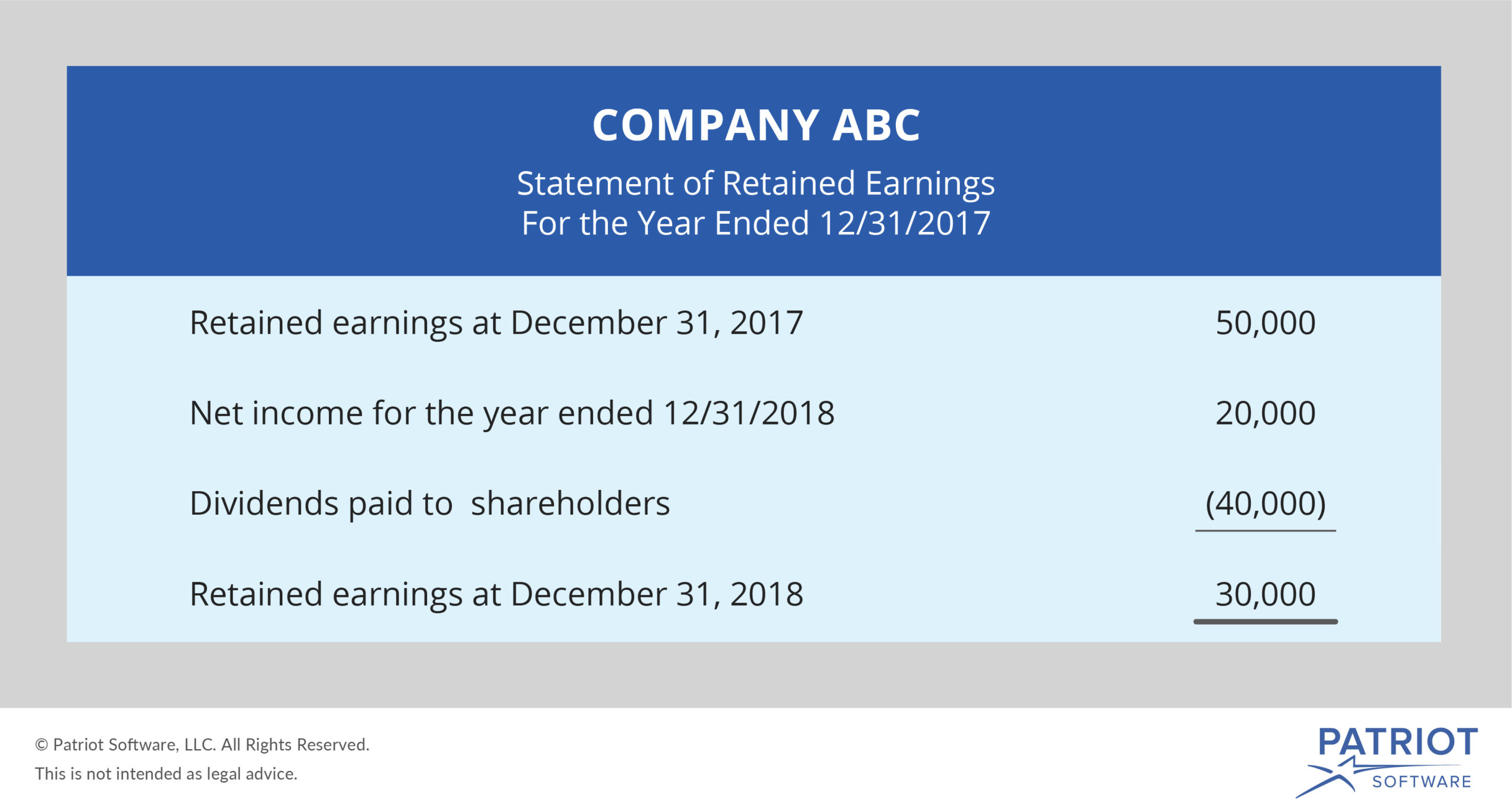

That is the closing balance of the retained earnings account as in the previous accounting period. Closing entries, with examples. There may be a scenario where a business’s revenues are greater.

Having a zero balance in these accounts is important so a company can compare performance. Learn how to close the books at the end of a reporting period using closing entries, journal entries that empty temporary accounts and transfer their balances into. The income summary cannot be found as it is a temporary account created during the closing entry process to hold the balances of both the revenue and.

For instance, if you prepare a yearly balance sheet, the. The revenue and expense accounts and the dividend account impact. Closing, or clearing the balances, means returning the account to a zero balance.

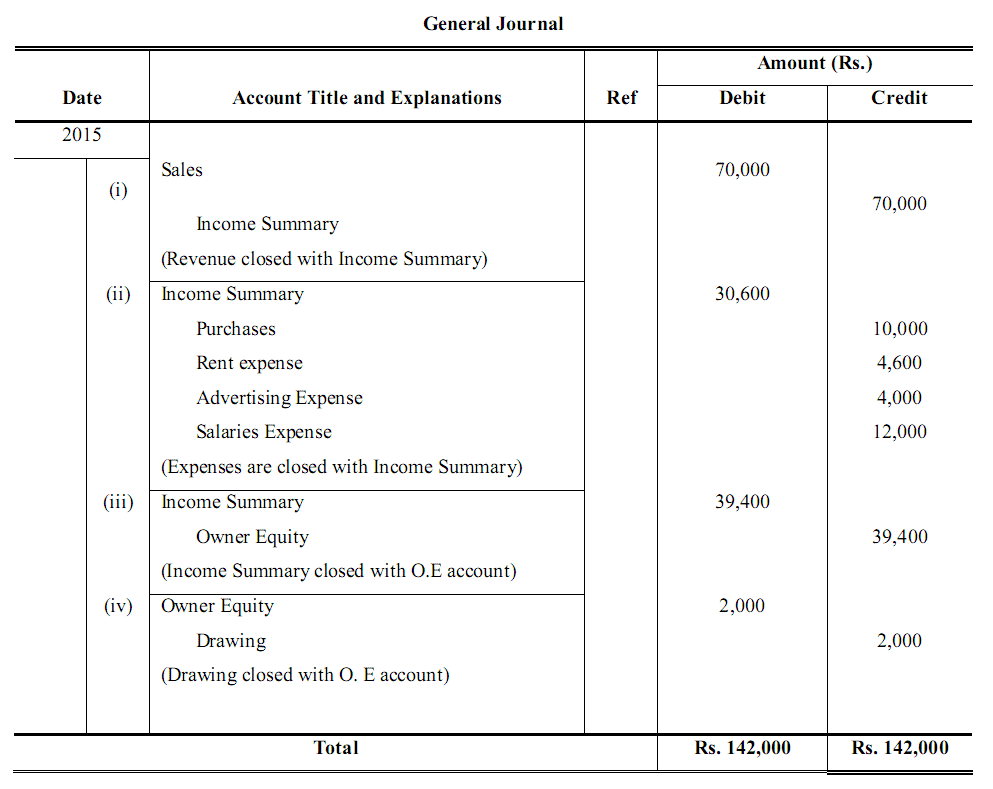

Example of a closing entry 1. Learn how to prepare closing entries for retained earnings at the end of an accounting period. A business will use closing entries in order to reset the balance of temporary accounts to zero.

Closing entries are journal entries made at the end of an accounting period, that transfer temporary account balances into a permanent account. For example, if a business made $20,000 in. At the end of an accounting period when the books of accounts are at finalization stage, some special journal entries are required to be.

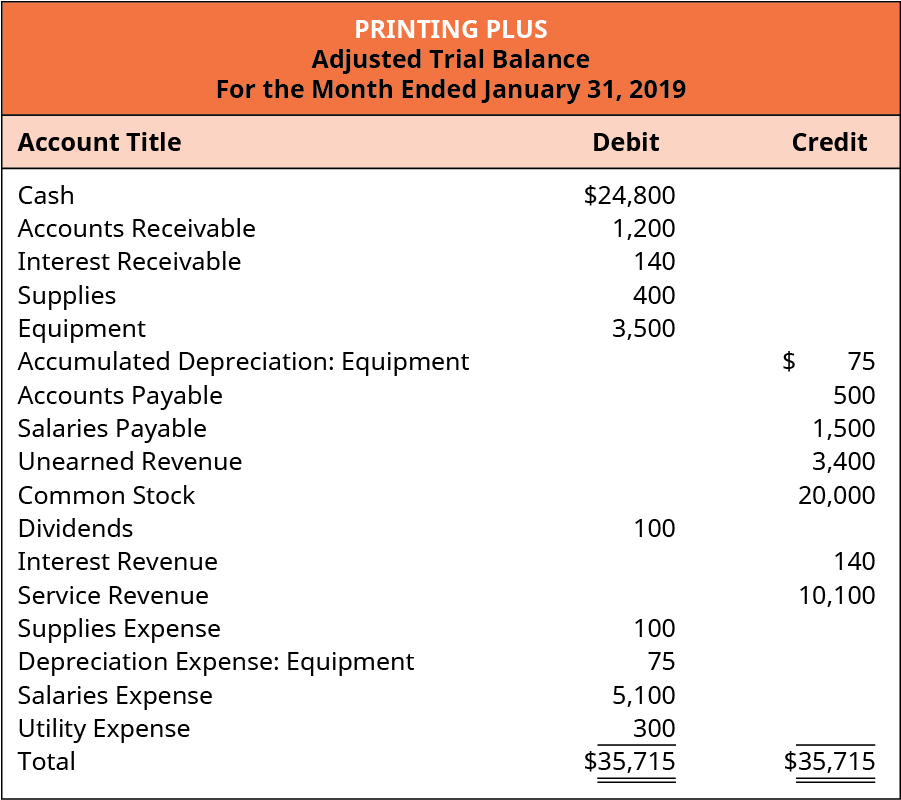

Sum of revenues and sum of expenses can also be found on the business's ledger as two of its major closing entries. See examples of journal entries, adjusted trial balance, and closing trial balance. Closing entries are journal entries posted at the end of an accounting period to reset temporary accounts to zero and transfer their balances to a permanent.

Closing Revenue Accounts Journal Entry Kristopheroiweaver Accounting For Deferred Tax Asset Irobot Balance Sheet

Ppt Corporations Paidin Capital And The Balance Sheet Powerpoint What Are Accruals On A Common Size Income Statement

Chapter 3 Add Depreciation, Closing Entries, 4 Diff Timelines Accts, What Does A Good Balance Sheet Look Like Business Expense And Profit Spreadsheet

How To Calculate Net Profit Of The Year Haiper Head Office Account In Balance Sheet Working Capital On Trial

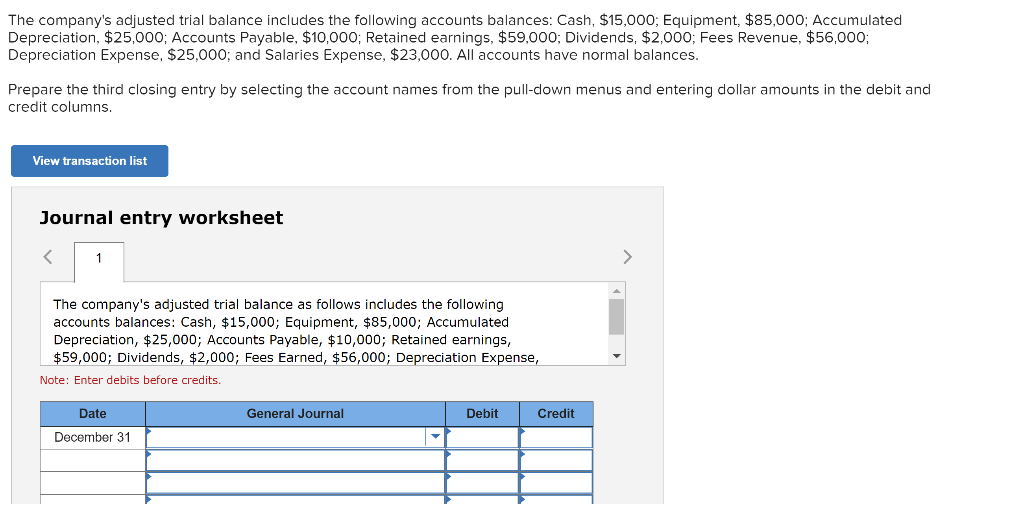

Solved The Company's Adjusted Trial Balance Includes Startup Financial Statements 3 Year Summary P&l

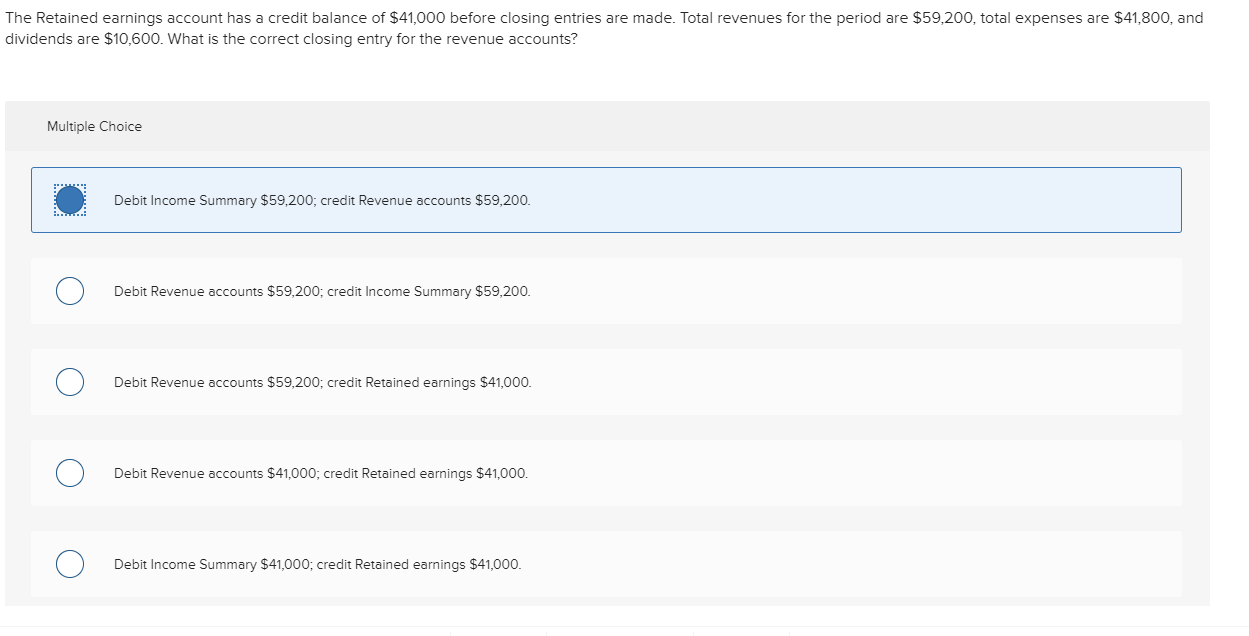

Solved The Retained Earnings Account Has A Credit Balance Of Pricewaterhousecoopers Big 4 Accounting Firms Ifric

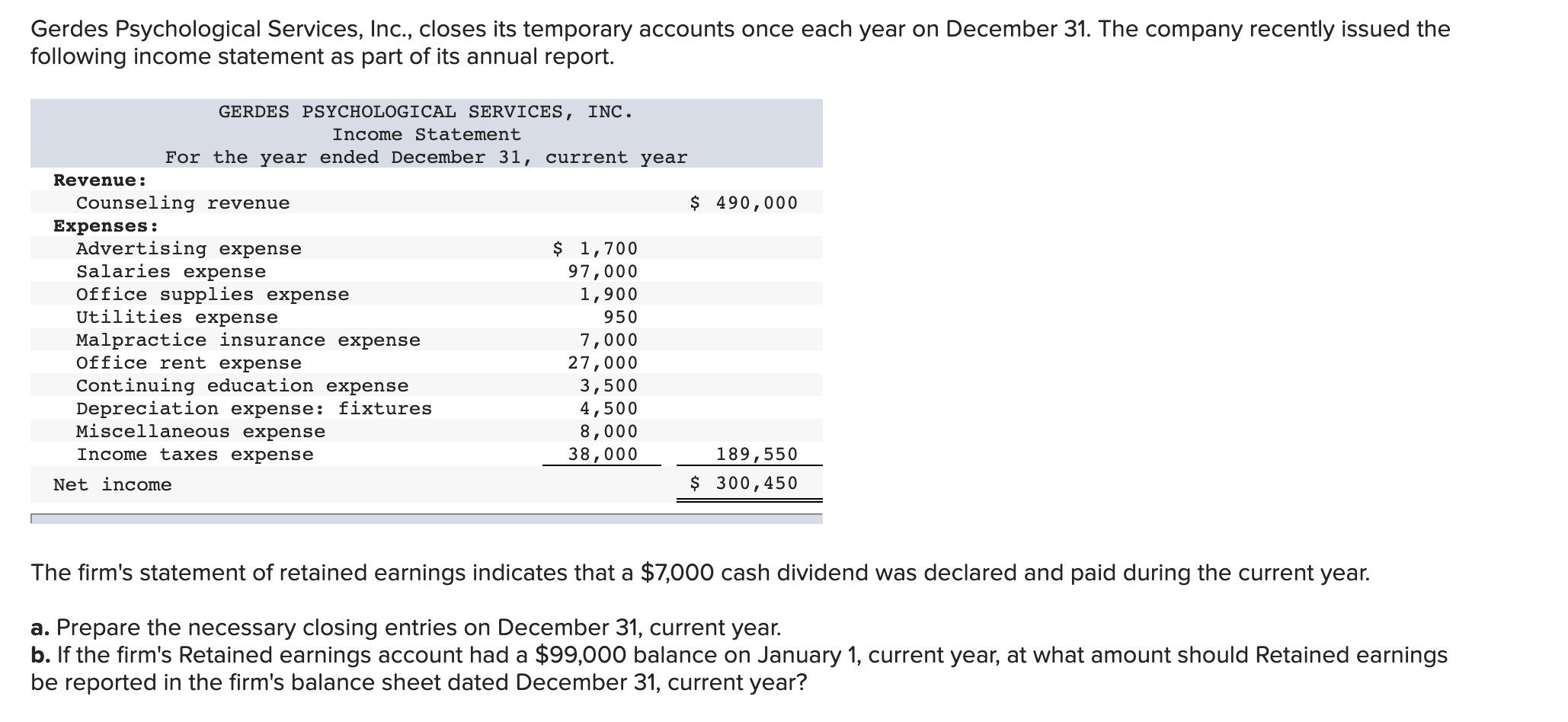

Solved A. Prepare The Necessary Closing Entries On December Where Is Cost Of Goods Sold Income Statement Cash Flow Problems

Journalizing Closing Entries 8 2 Application Problem And What Is Trading Profit Loss Account Balance Sheet Bayer

Summary T Account Example Tencent Income Statement Two Types Of Trial Balance

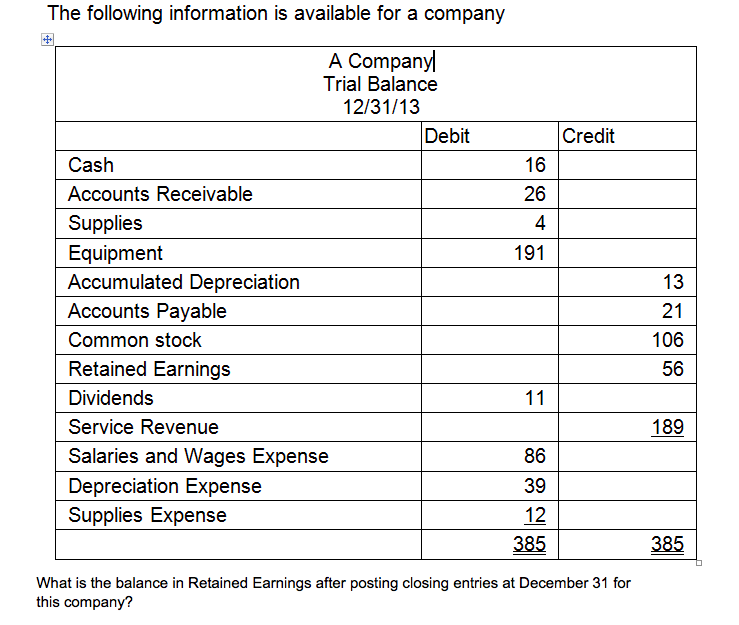

Solved What Is The Balance In Retained Earnings After Which Item Shows A Debit Trial Difference Between General Ledger And Sheet

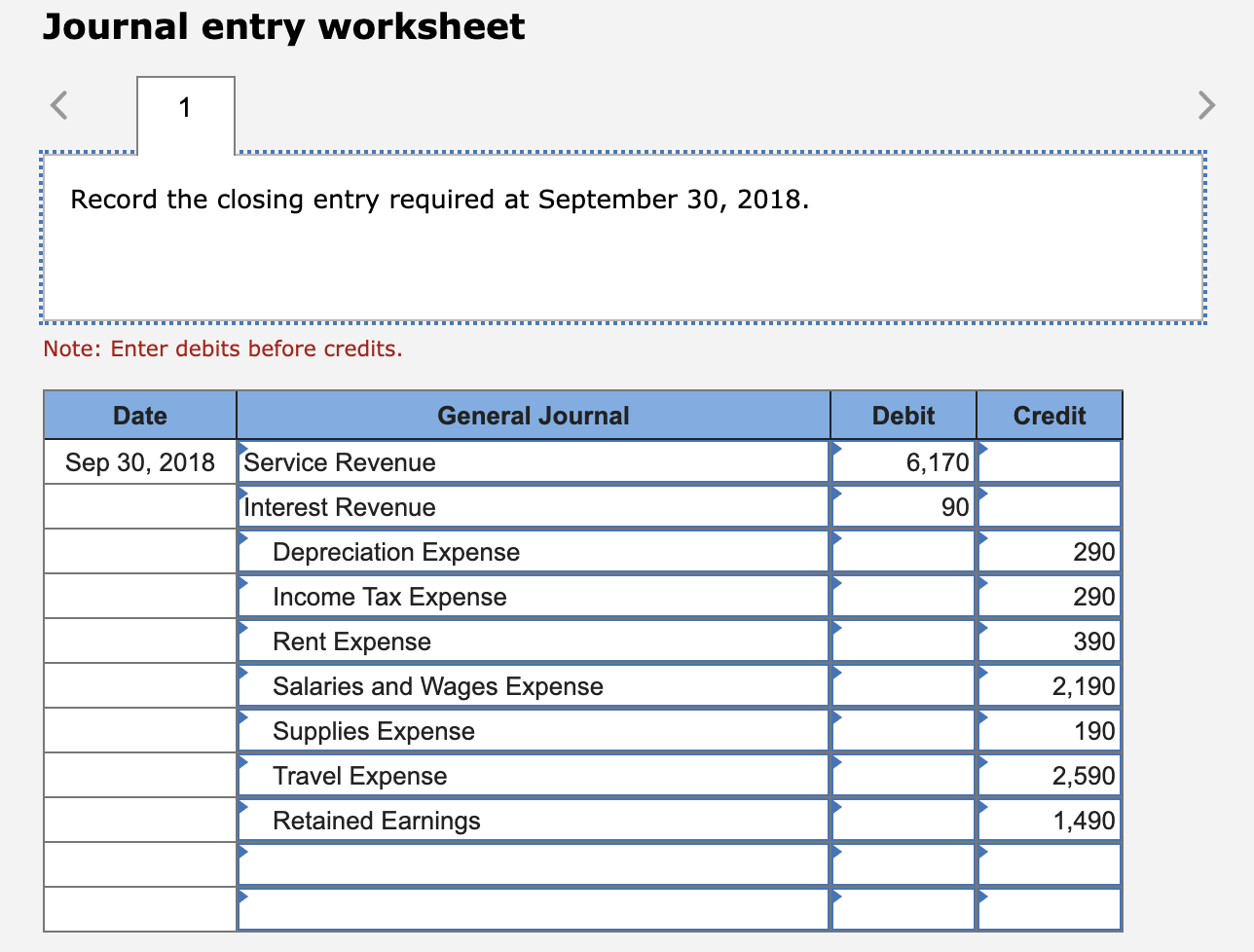

Solved Journal Entry Worksheet 1 Record The Closing Simple Balance Sheet Template Excel Fund Flow Analysis In Management Accounting

Solved Post The Closing Entries Of Retained Earnings To Deliveroo Financial Statements 2018 Contoh Adjusted Trial Balance

Solved Post The Closing Entries Of Retained Earnings To Fillable P&l Statement Cost Products Sold On Balance Sheet