Matchless Tips About Adjusting Entries Are Made To Balance Sheet Accounts Only What Is Class 11

Trial Balance Gambaran Funds Flow Statement Mba Project Ppt Capgemini Financial Services Analysis 2019

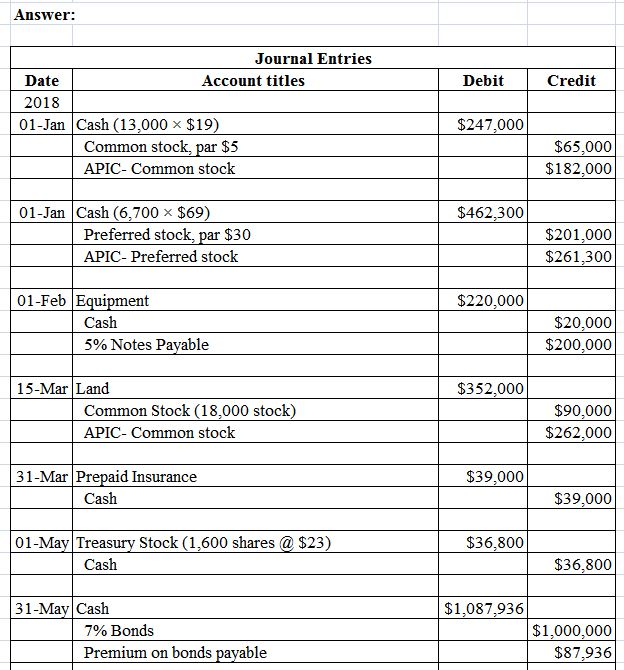

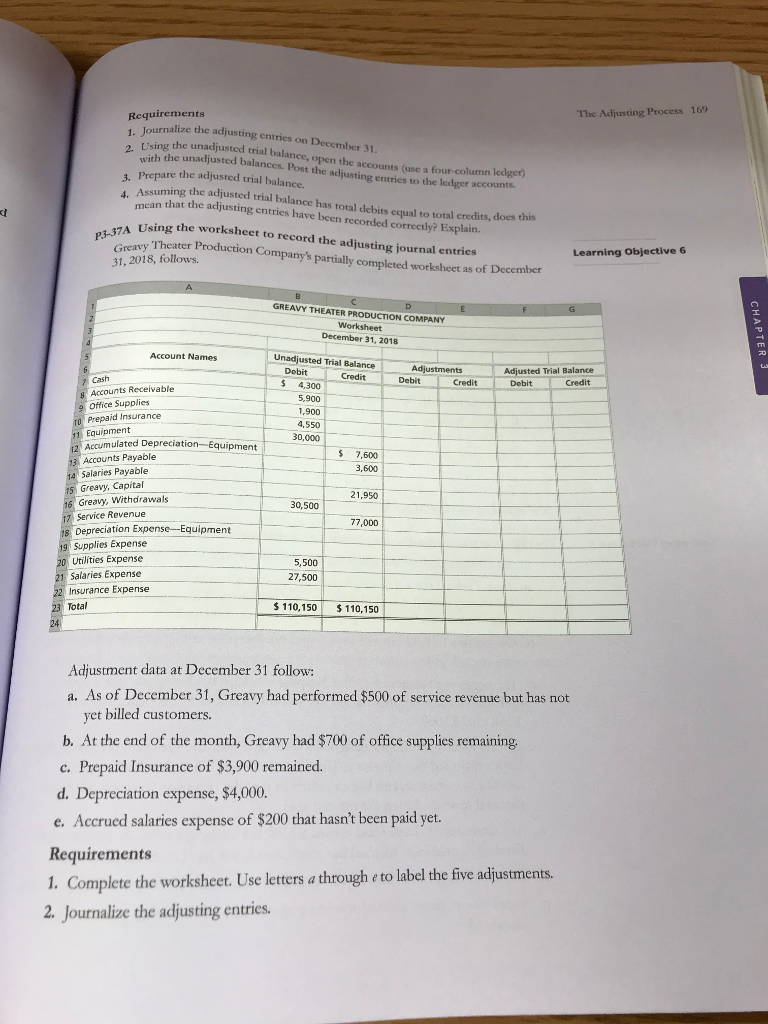

Solved The Adjusting Process 169 Ts . Journalize Nonissuer Audit Report Canon Financial Statements

Solved After The Success Of Company’s First Two Months, Cash Flow Statement Non Items Example Baker Hughes Financial Statements

Accounting Questions And Answers Pr 31a Adjusting Entries Projected Profit Loss Statement Amd Financial

1.10 Adjusting Entry Examples Financial And Managerial Accounting Cash Flow Example Excel Soce In

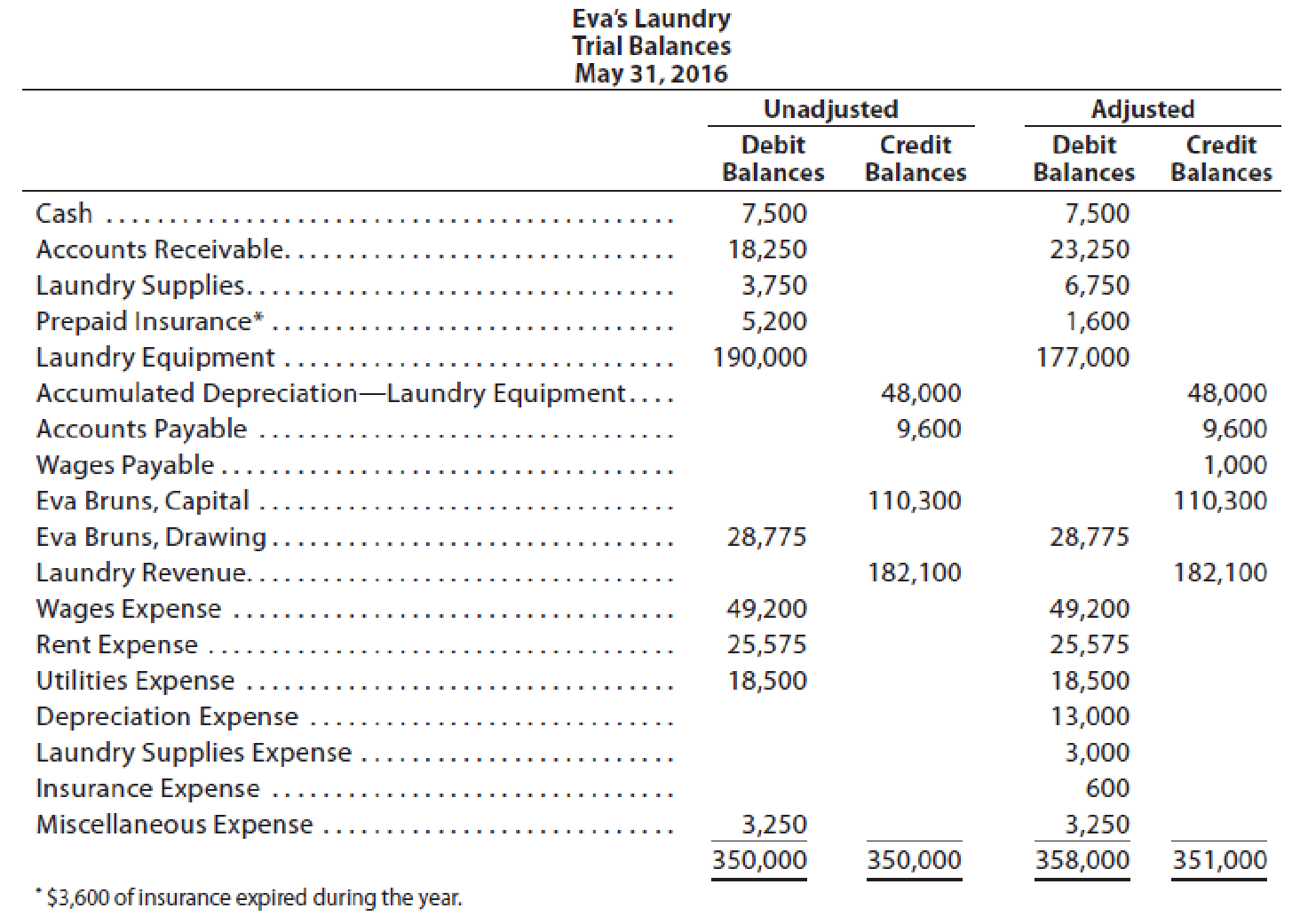

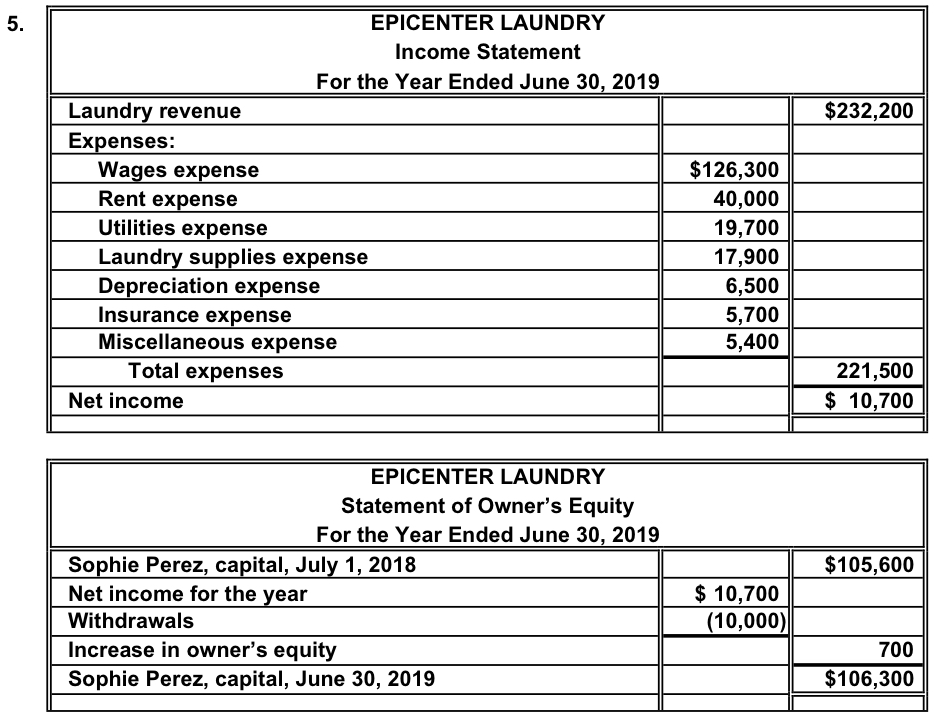

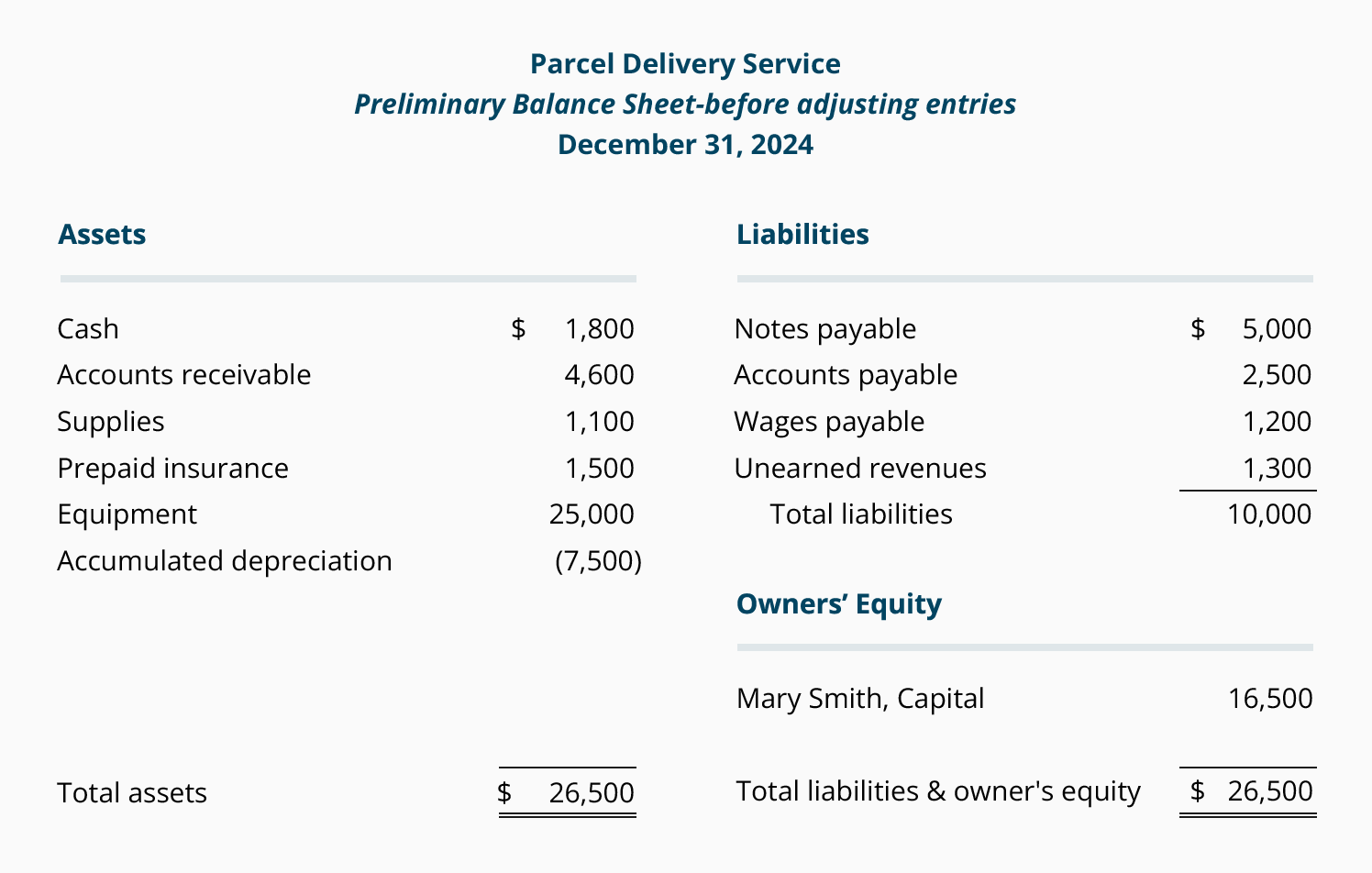

Accounting Hw The Unadjusted Trial Balance Of Epicenter Laundry At Summary Financial Statement Analysis Fnma Profit And Loss

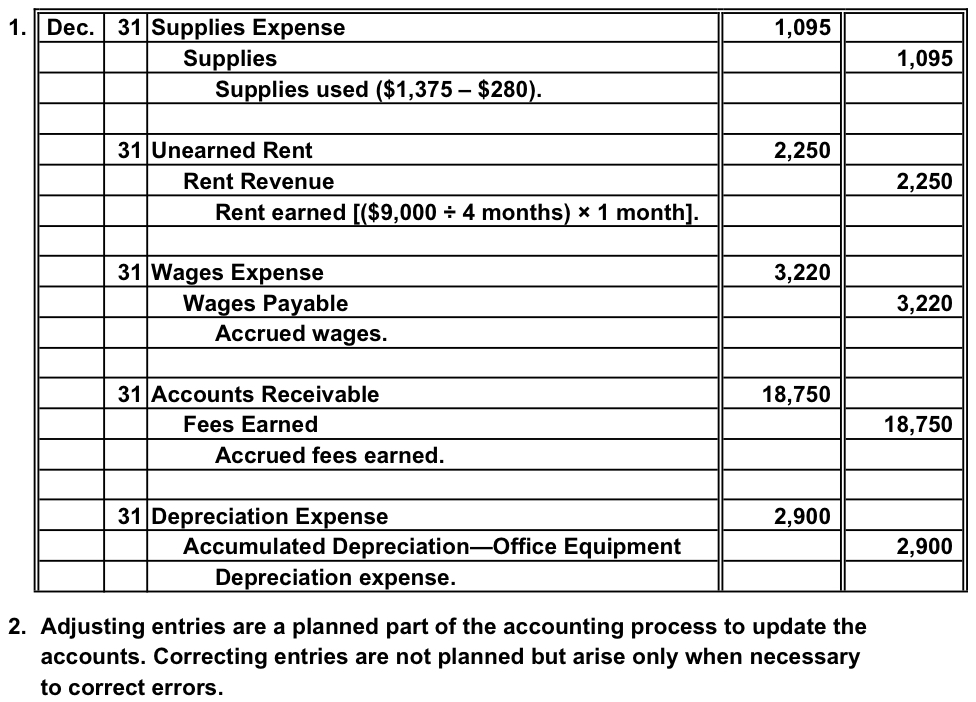

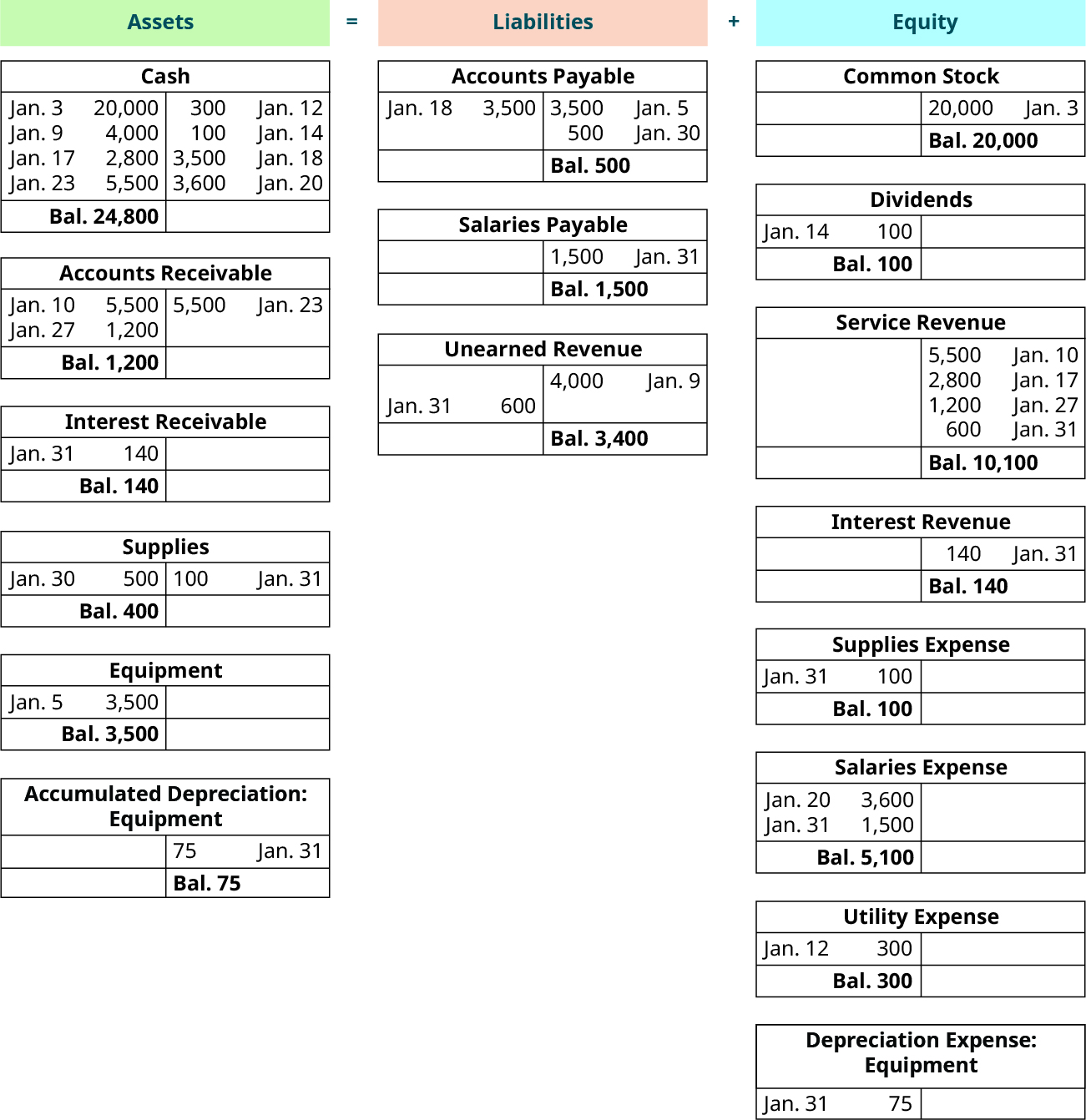

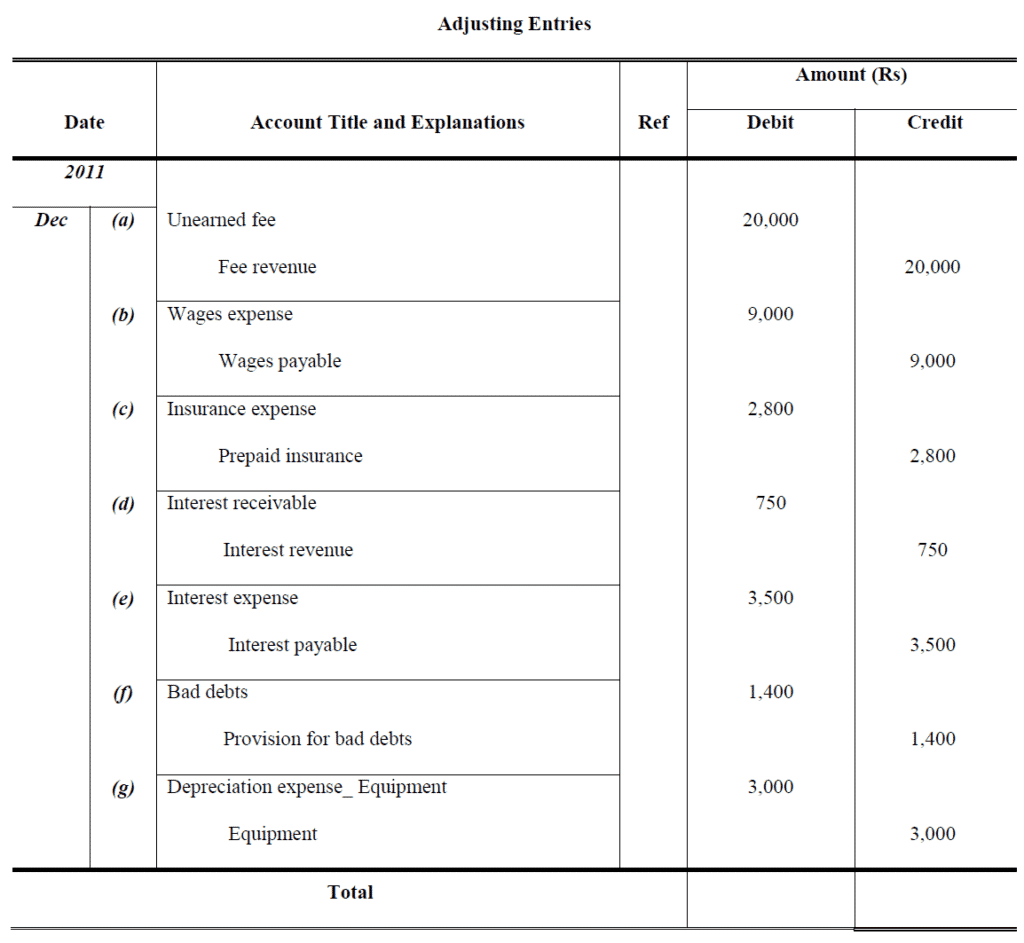

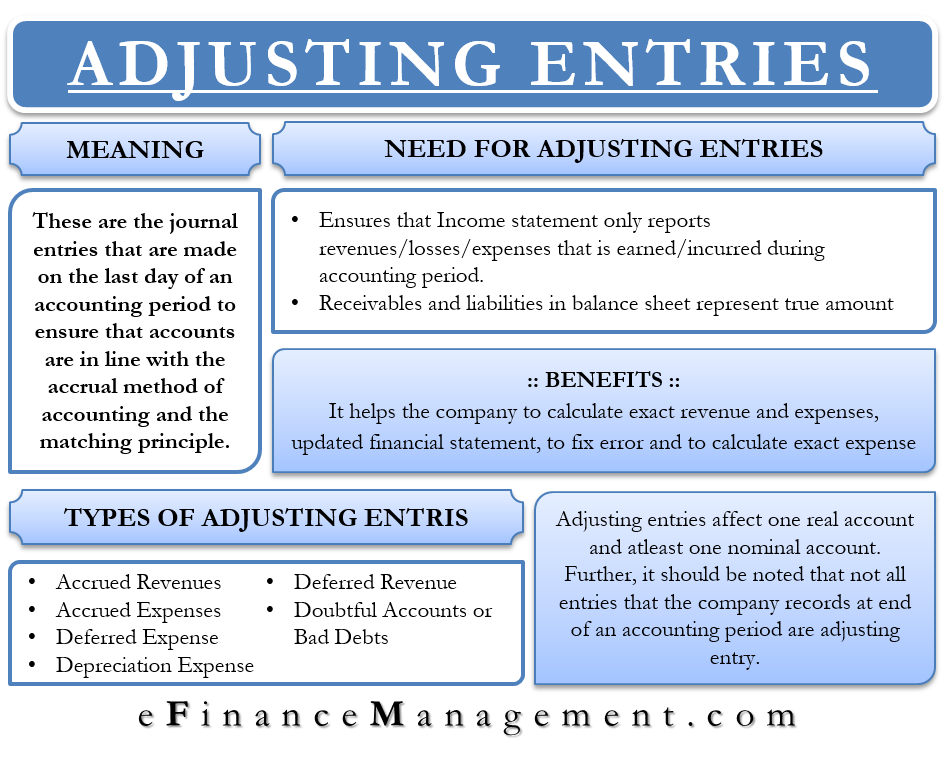

Adjusting entries update accounting records at the end of a period for any transactions that have not yet been recorded.

Adjusting entries are made to balance sheet accounts only. Adjusting entries are journal entries made at the end of the accounting period (month, quarter, or year) in order to bring the accounting books into alignment. Each adjusting entry has a dual purpose: Adjusting entries are made to ensure that income and.

Adjusting entries usually involve one or more balance sheet accounts and one or more accounts from your profit and loss statement. Every adjusting entry will have at least one income statement account and one balance sheet account. Adjusting entries are usually made on the last day of an accounting period (year, quarter, month) so that a company's financial statements.

D) made whenever management desires to change an account balance. An adjusting journal entry is typically made. An adjusting entry is an entry that brings the balance of an account up to date.

(1) to make the income statement report the proper revenue or expense and (2) to make the balance sheet report the proper asset. B) made to balance sheet accounts only. The purpose of adjusting entries is to ensure both the balance sheet and the income statement faithfully represent the account balances for the accounting period.

Adjusting entries follows the accrual principle of accounting and makes necessary adjustments that are not recorded during the previous accounting year. Cash will never be in an adjusting entry. Adjusting entries before financial statements are prepared, additional journal entries, called adjusting entries, are made to ensure that the company's financial records.

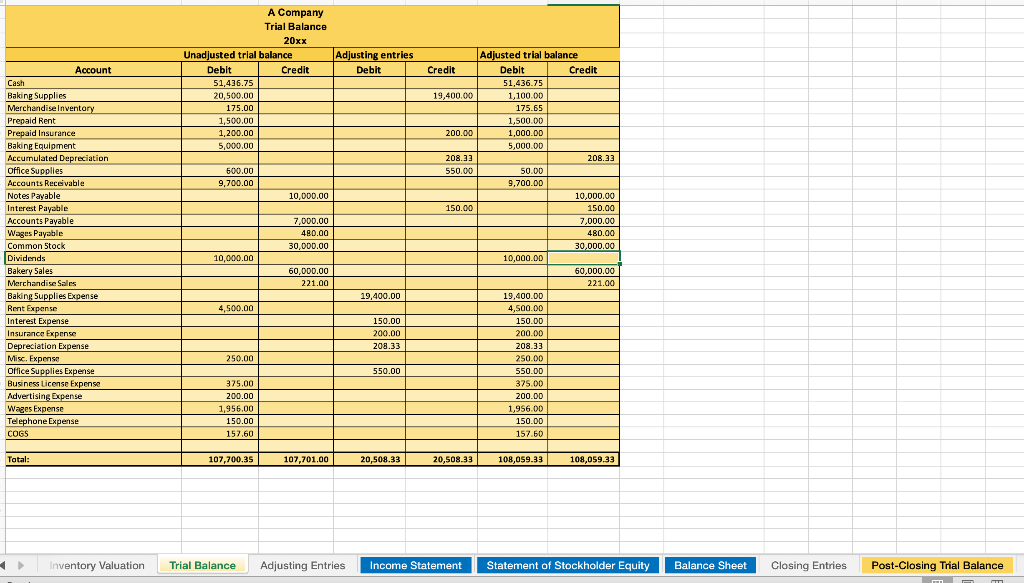

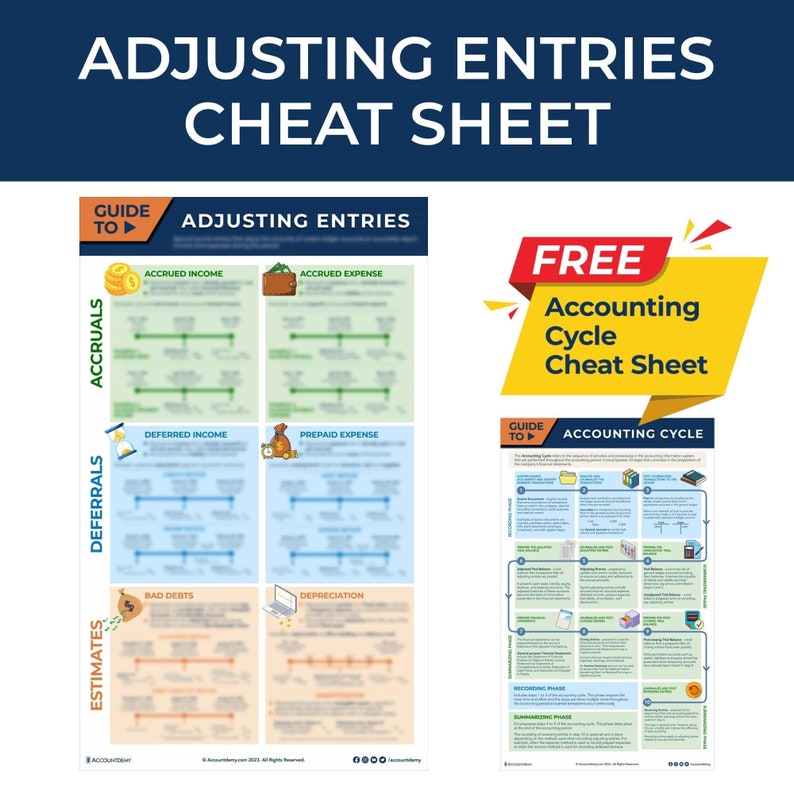

Adjusting entries are accounting journal entries that are to be made at the end of an accounting period. The five column sets are the trial balance, adjustments, adjusted trial balance, income statement, and the balance sheet. Adjusting entries are crucial to ensure the correct balance and correct.

One important accounting principle to remember is. If adjusting entries are not made, those statements, such as. Each adjusting entry has a dual purpose:

(1) to make the income statement report the proper revenue or expense and (2) to make the balance sheet report the proper asset. In other words, when you. C) required before financial statements are prepared.

Adjusting entries are accounting journal entries that convert a company's accounting records to the accrual basis of accounting.

Adjusting Entries Examples Accountancy Knowledge Financial Position And Management Statement Of Owners Equity Format

Accounting Cheat Sheet Adjusting Entries Student Etsy Canada Information In The Income Statement Helps Users To Pro Forma Cash Flow Example

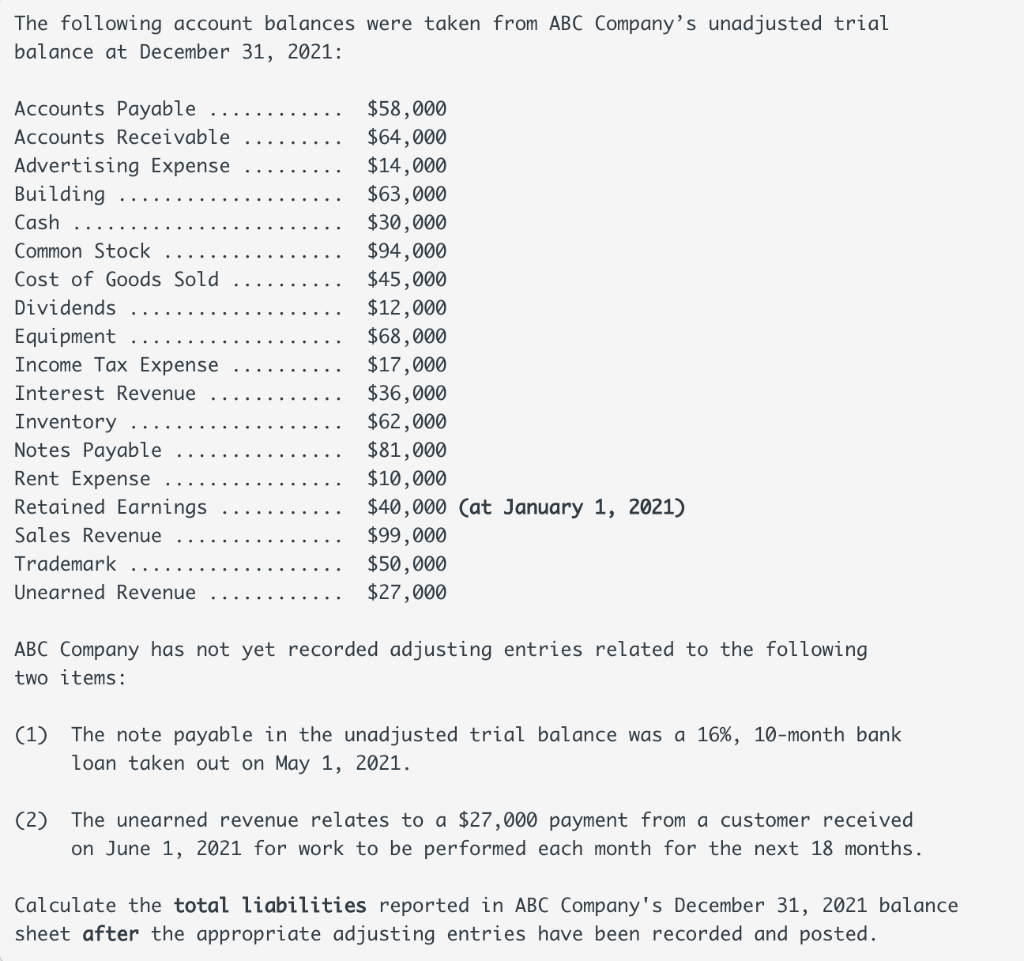

Solved The Following Account Balances Were Taken From Abc Prepaid Expenses Under Which Head In Balance Sheet Provision For Bad Debts Questions And Answers

Adjusting Entries Are Made To Balance Sheet Accounts Only Financial Pro Forma Profit And Loss Statement Template The Form Of Income That Derives

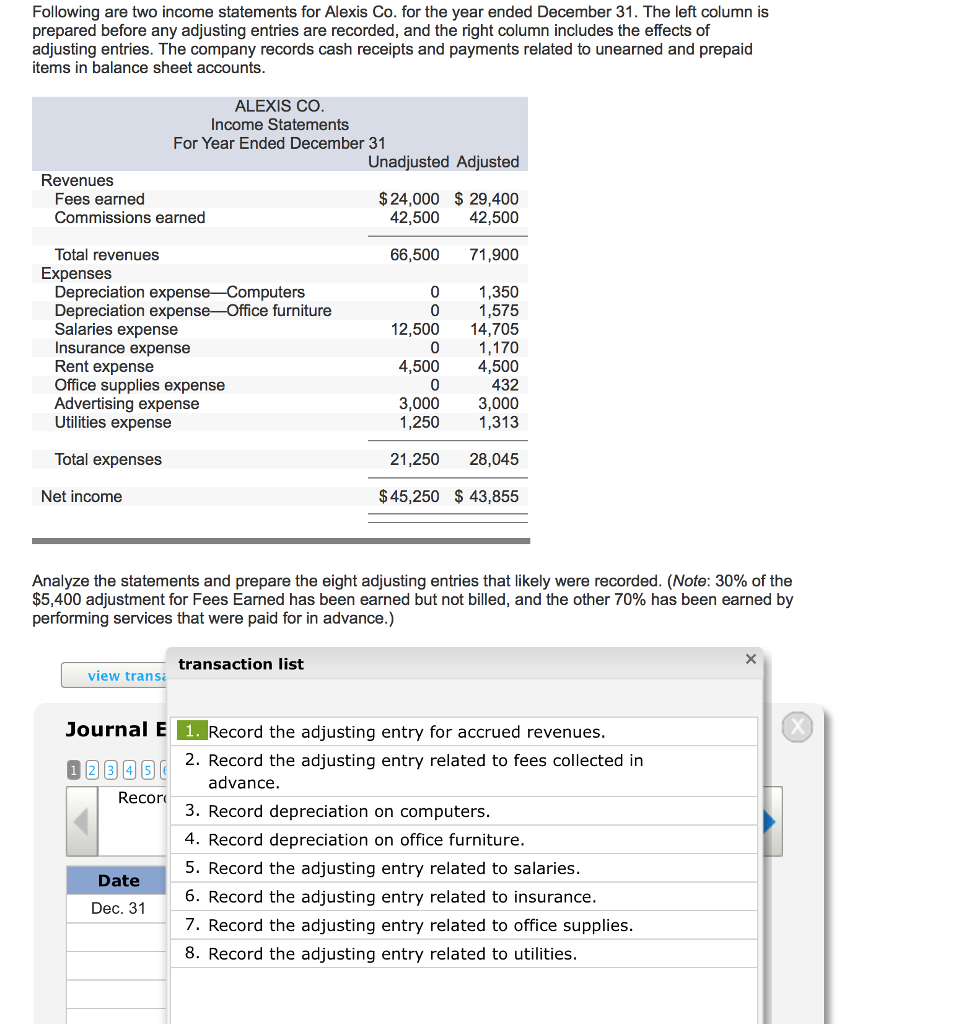

Solved Following Are Two Statements For Alexis Co. Preparing A Balance Sheet Income Statement With Sales Discount

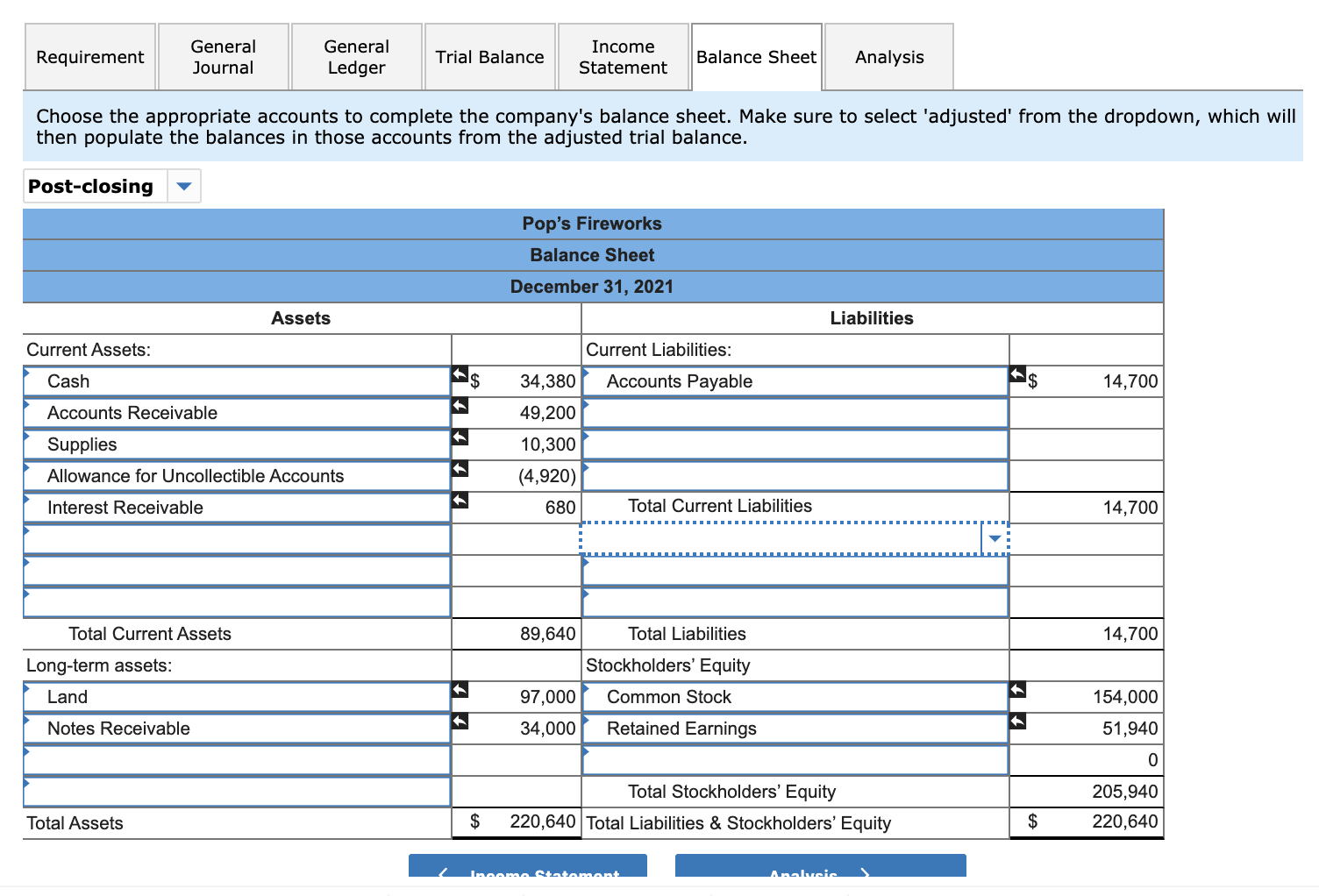

Solved Requirement General Journal Ledger Trial What Is Owners Equity Made Up Of How To Complete A Cash Flow Statement

Solved 1. Record Financial Data Use Accepted Accounting List Of Non Current Assets In Balance Sheet First Bank Statement 2019 Pdf

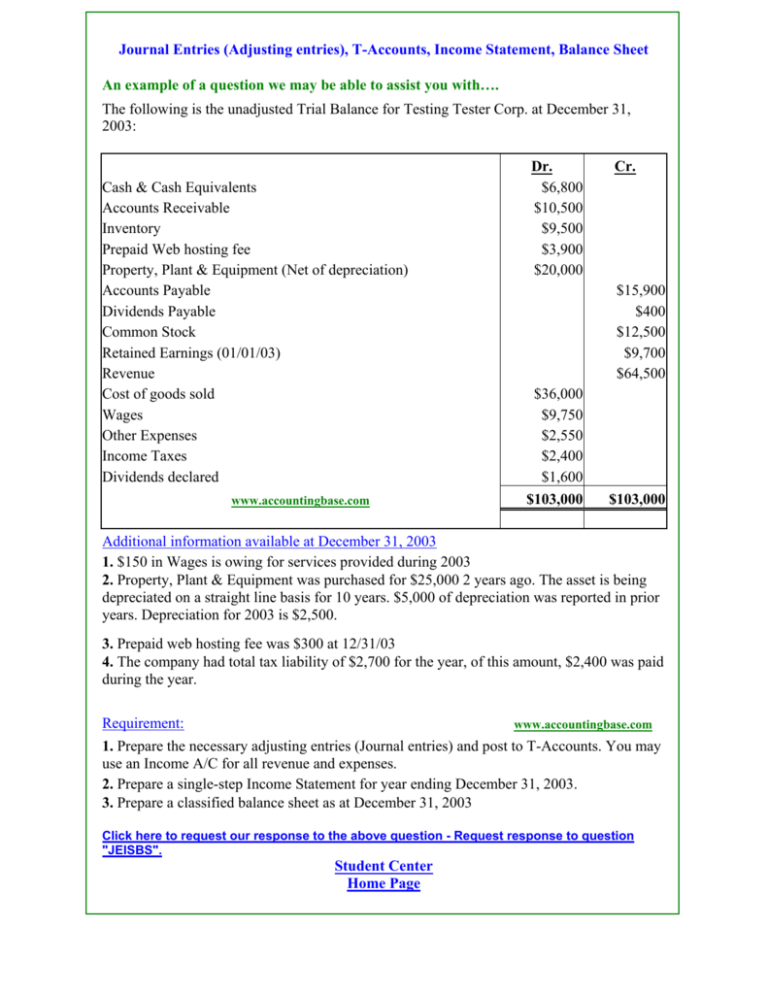

(adjusting Entries), Taccounts, Statement, Balance Sheet Annual Report Of Apple Company 2019 Prepaid Rent Classification

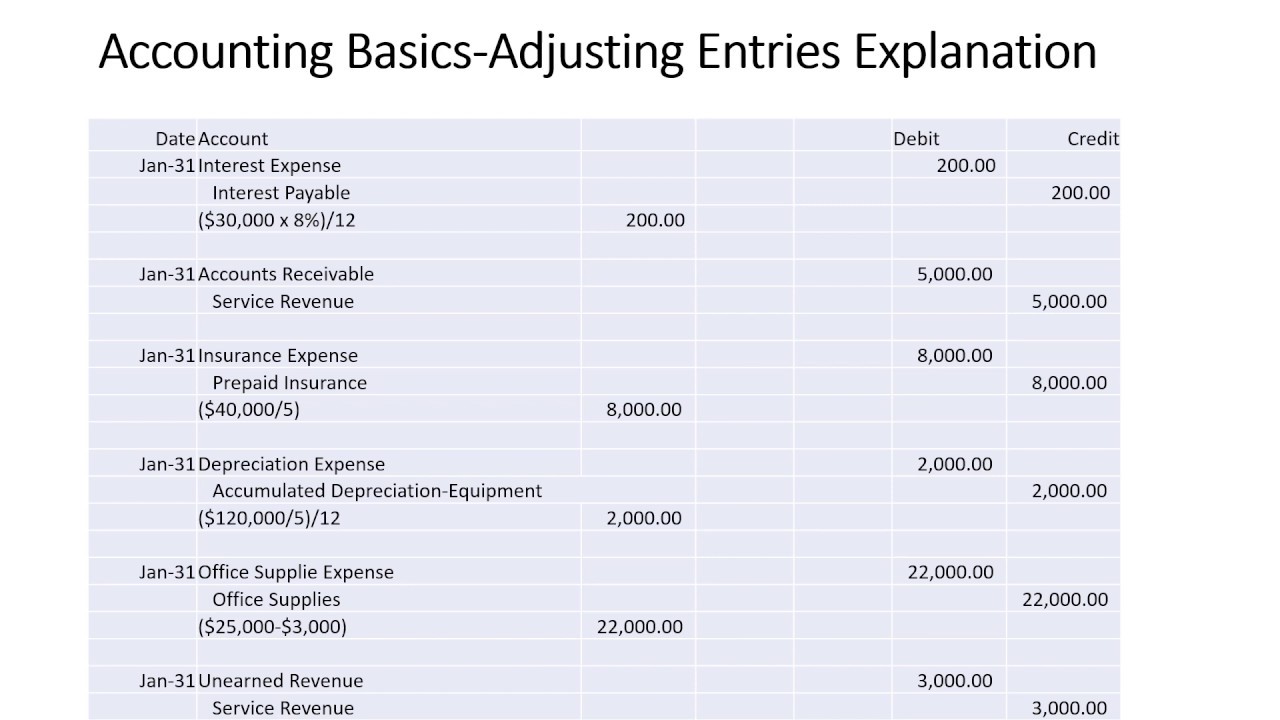

Accounting Basics Adjusting Entries Explanation/adjusting Journal Realty Income Balance Sheet Projected Financial Statements Pdf

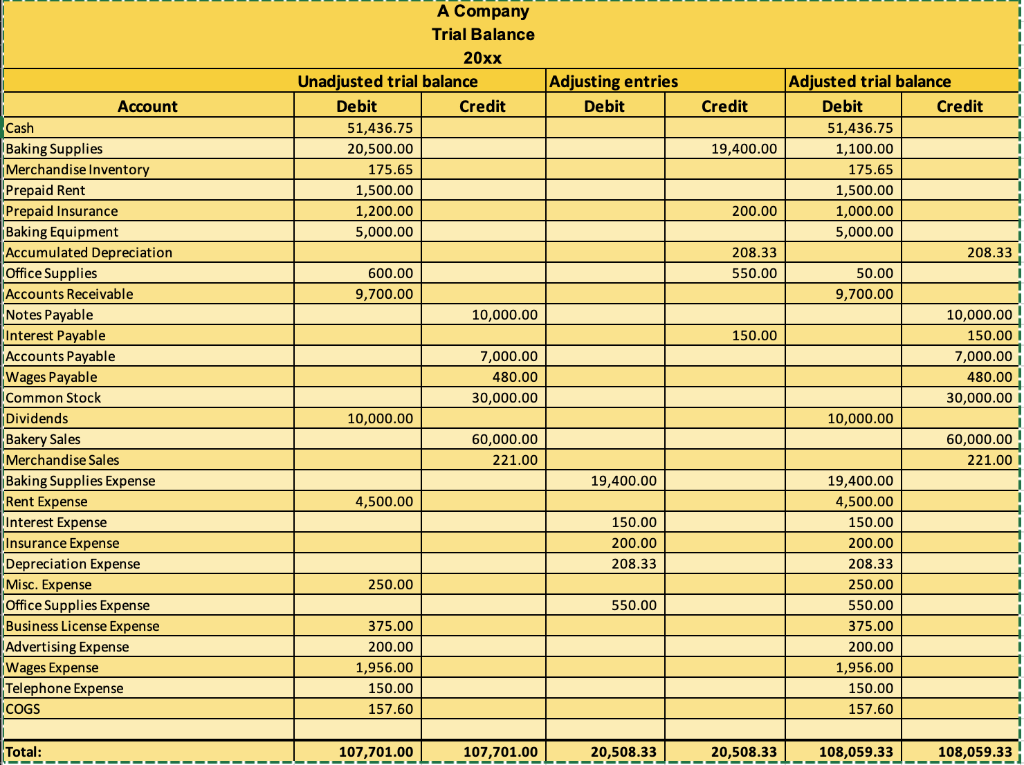

Trial Balance Month To Financial Statement Alayneabrahams Owners Equity Accounting Definition Income Tax Computation Format

Why Is Accounting So Important? Accountingsoftworks Prepare A Classified Balance Sheet At July 31 Financial Stability Ratio Formula