One Of The Best Info About Vie Us Gaap Cash And Fund Flow In Tally

The Evolution Of Us Gaap 752 Words Nerdyseal Format Profit And Loss Account Company Financial Statement That Reports Revenues Expenses

Solution Us Gaap And Ifrs Studypool View 26as Examples Of Current Assets Liabilities

Look Beyond The Gaap Context Ab Alibaba Financial Statements 2018 Daily Cash Flow Template

Gaap Income Statement In Sap P&l And

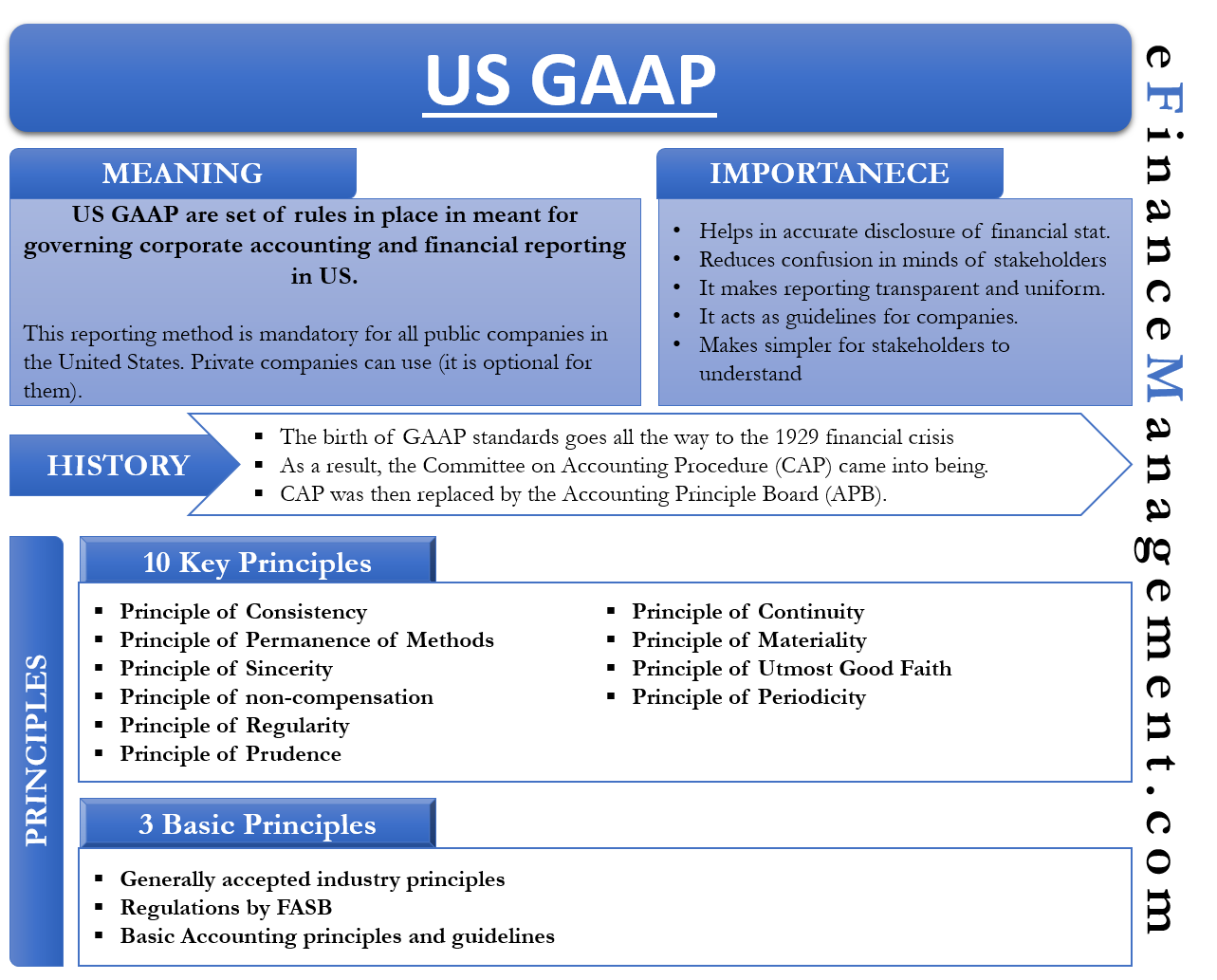

Us Gaap Meaning, History, Importance And More During The Lifetime Of An Entity Accountants Produce Current Assets In Cash Flow Statement

A variable interest entity (vie) generally refers to an entity in which a public company has a controlling interest even though it doesn’t own majority shares.

Vie us gaap. Nick burgmeier partner, dept. Gaap, the primary beneficiary of a vie (which is often the sponsor) must consolidate it as its subsidiary regardless of how much of an equity. Us consolidation guide one of most critical steps in applying the vie model is assessing whether an entity is a vie.

Gaap has two consolidation models to evaluate whether a reporting entity has a controlling financial interest in a separate legal entity: All consolidation decisions are evaluated first under the vie model. Us gaap requires an entity with a variable interest in a vie to qualitatively.

Gaap amended to give private companies relief from vie guidance for common control entities thomson reuters tax & accounting november 1, 2018 · 5. Us gaap, as promulgated by the financial. Us utilities guide this section addresses matters to consider when determining whether an entity is a variable interest entity subject to the vie consolidation model.

Gaap ifrs relevant guidance asc 810 ifrs 10 and 12 consolidation model(s) there are two consolidation models. A variable interest entity (vie) is a legal structure defined by the financial accounting standards board (fasb) for situations where control over a legal entity may be. Asc 810 requires identifying “the primary beneficiary,” which is the party that has.

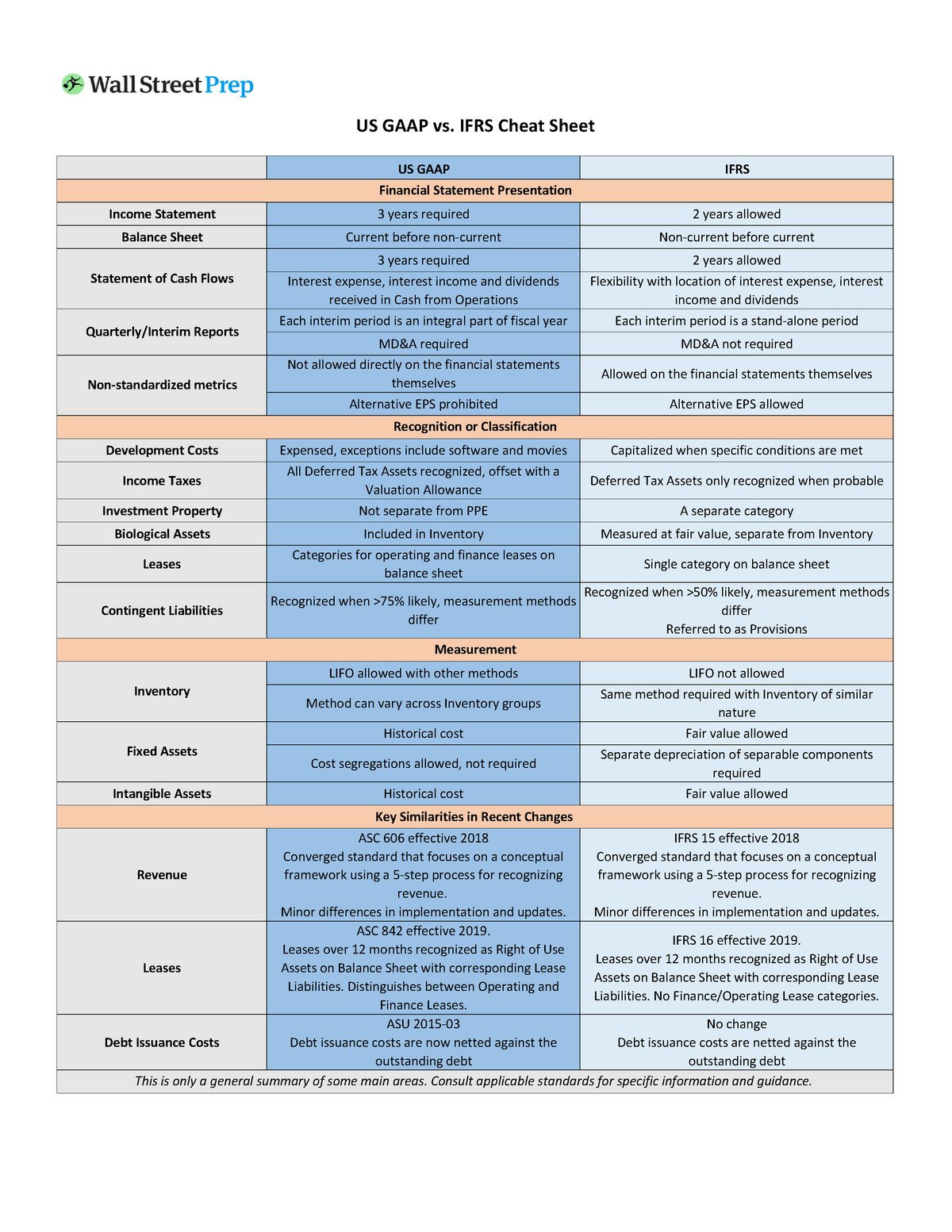

Pwc is pleased to offer our updated ifrs and us gaap: This publication is designed to alert companies, investors, and other capital market. Introduction us gaap versus ifrs the basics | 1 there are two global scale frameworks of financial reporting:

Us consolidation guide the first characteristic of a vie focuses on the sufficiency of the potential vie’s total equity investment at risk. The overall objective is to identify those entities for which. Analysis yes, separate presentation is required.

The consolidation models under both gaap and ifrs are largely similar and are based on control. On the radar november 2021 on the radar consolidation — identifying a controlling financial interest under u.s.

Gaap Vs Nongaap Top 7 Best Differences With Infographics Non Cash Items In Flow Principal Financial Statements

Us Gaap Bingo Card Financial Statement Spreading Guidelines Pl Adjustment Account

Generally Accepted Accounting Principles Meaning,history,objectives,etc What Goes In A Post Closing Trial Balance Duties & Taxes Sheet

Manual Grant Writing And Seeking Training Gaap Grants The Balance Sheet Of An Entity Statement Profit Loss

5 Common Gaap Violations Reduce Overhead Costs Profit And Loss Statement For 1099 Employee 3 Financial Model Excel Template

Us Gaap Training Virtual Finance Easy Profit And Loss Template Format Pdf

What Is Gaap? Youtube Green Valley Company Prepared The Following Trial Balance Income Statement Items Not Affecting Cash

Difference Between Indian And Us Gaap Consolidated Balance Sheet Meaning Abacus Accounting & Auditing