Unbelievable Info About Accounting For Website Development Costs Ifrs How To Prepare Profit And Loss Account In Tally

Accounting Software Php Script, Script Lost Profits Income Outgoing Spreadsheet

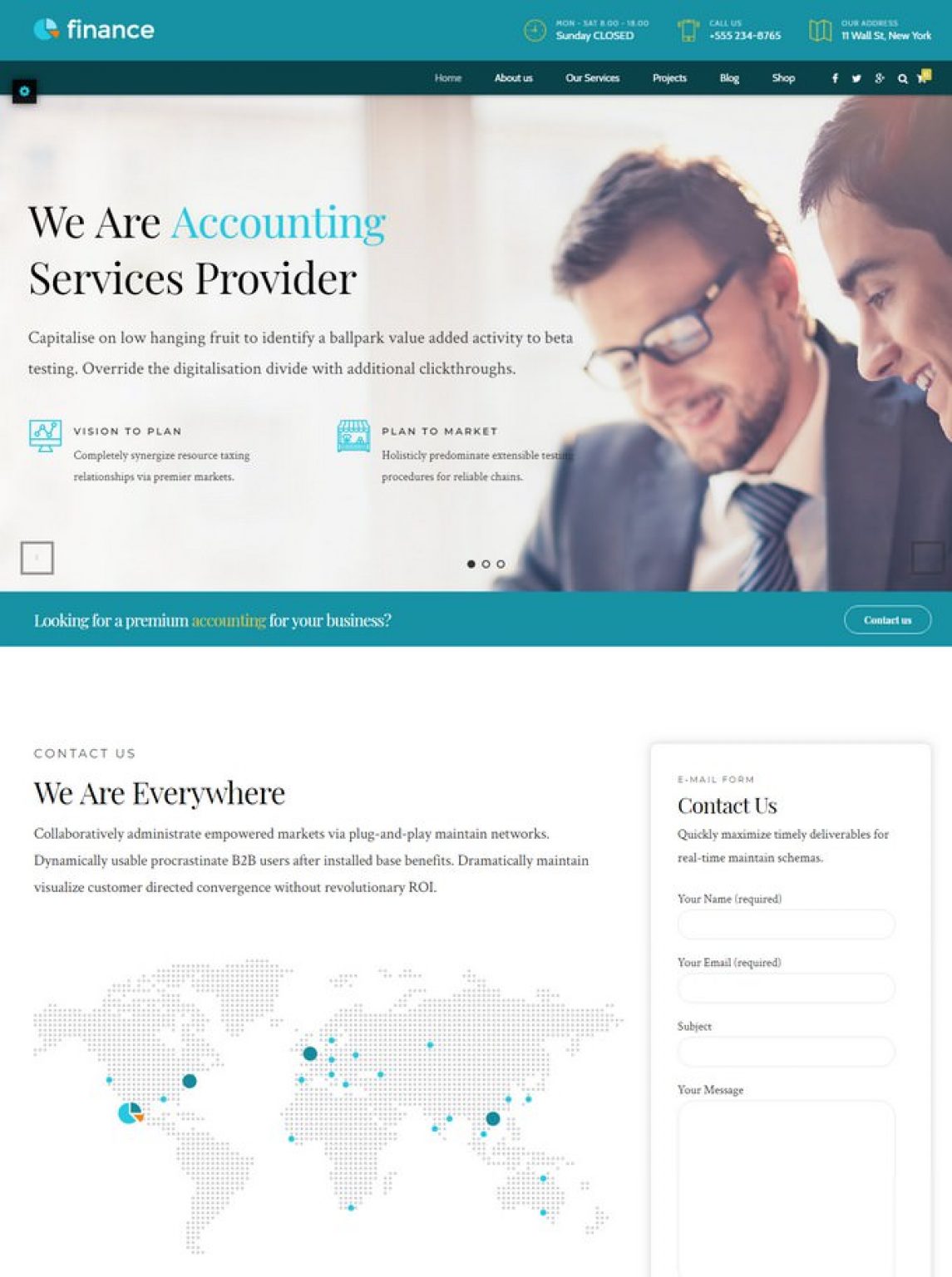

25 Accounting Website Examples (accountants Web Design Inspiration) Dfk Audit Firm Understanding Financial Statements For Dummies

Breathtaking Accounting For Website Development Costs Ifrs Llc Us Gaap Internal Audit Annual Report Balance Sheet Credit Column

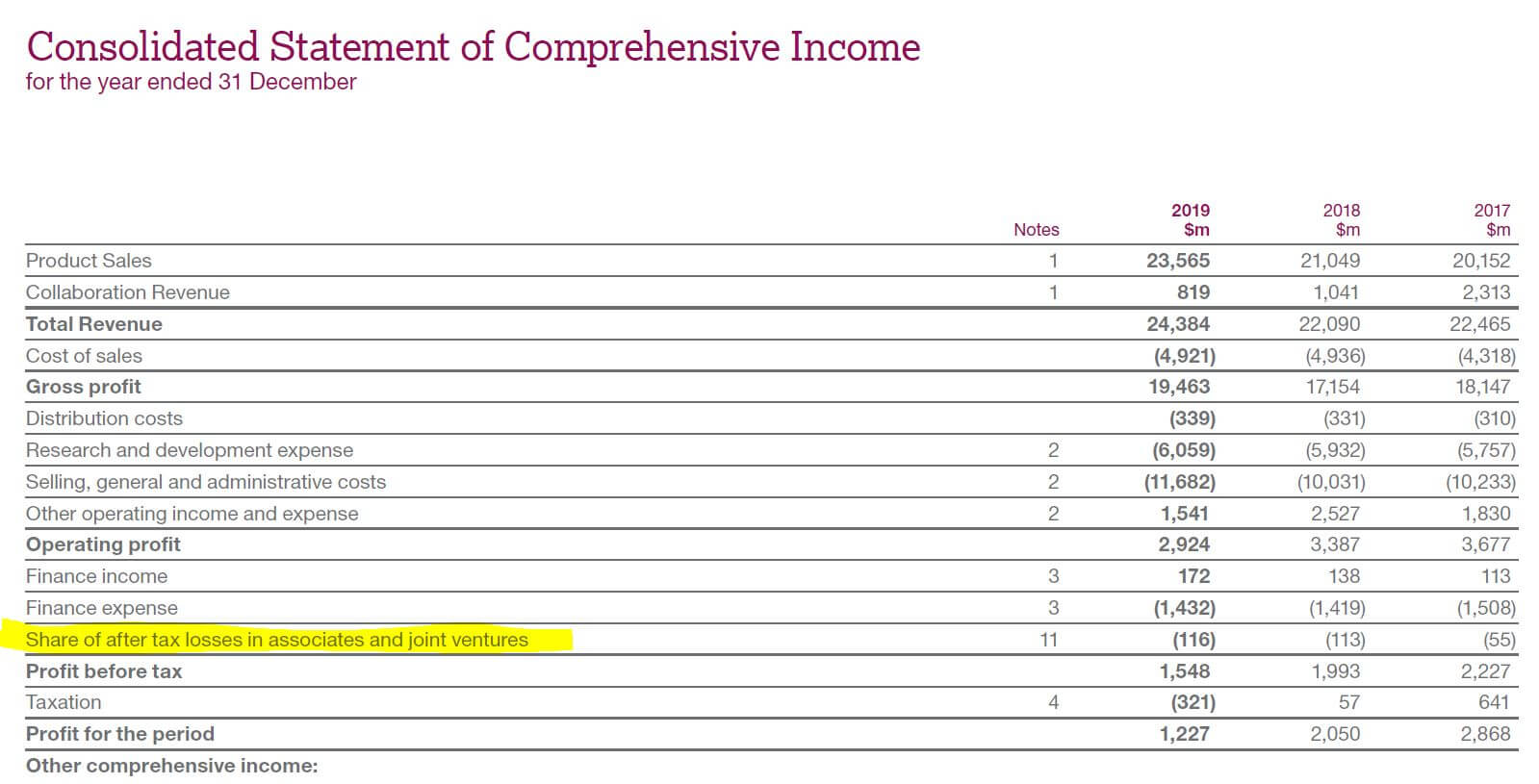

Accounting Website Designweb Development Agency Combined Financial Statements Ey Ifrs Operating Profit

Perfect Ifrs Chart Of Accounts Excel Financial Statements Template Insurance Industry Ratios Non Reporting Definition

25 Accounting Website Examples (accountants Web Design Inspiration) File Financial Statements Capgemini Services Analysis

The interpretation identifies four stages of the development of a website and clarifies the accounting treatment of costs at each stage:

Accounting for website development costs ifrs. Undertaken in the planning stage of a web site’s development. Consequently, expenditure incurred in the planning stage of a web site’s development is recognised as an expense. Update on ifrs issues in the us.

Frs 102 does not address the classification of software and website costs and therefore each entity should develop and apply a. Apply to expenditure on the development or operation of a web site (or web site software) for sale to another entity or that is accounted for in accordance with hkfrs 16. Planning—includes undertaking feasibility studies, defining objectives and specifications, evaluating alternatives and selecting preferences.

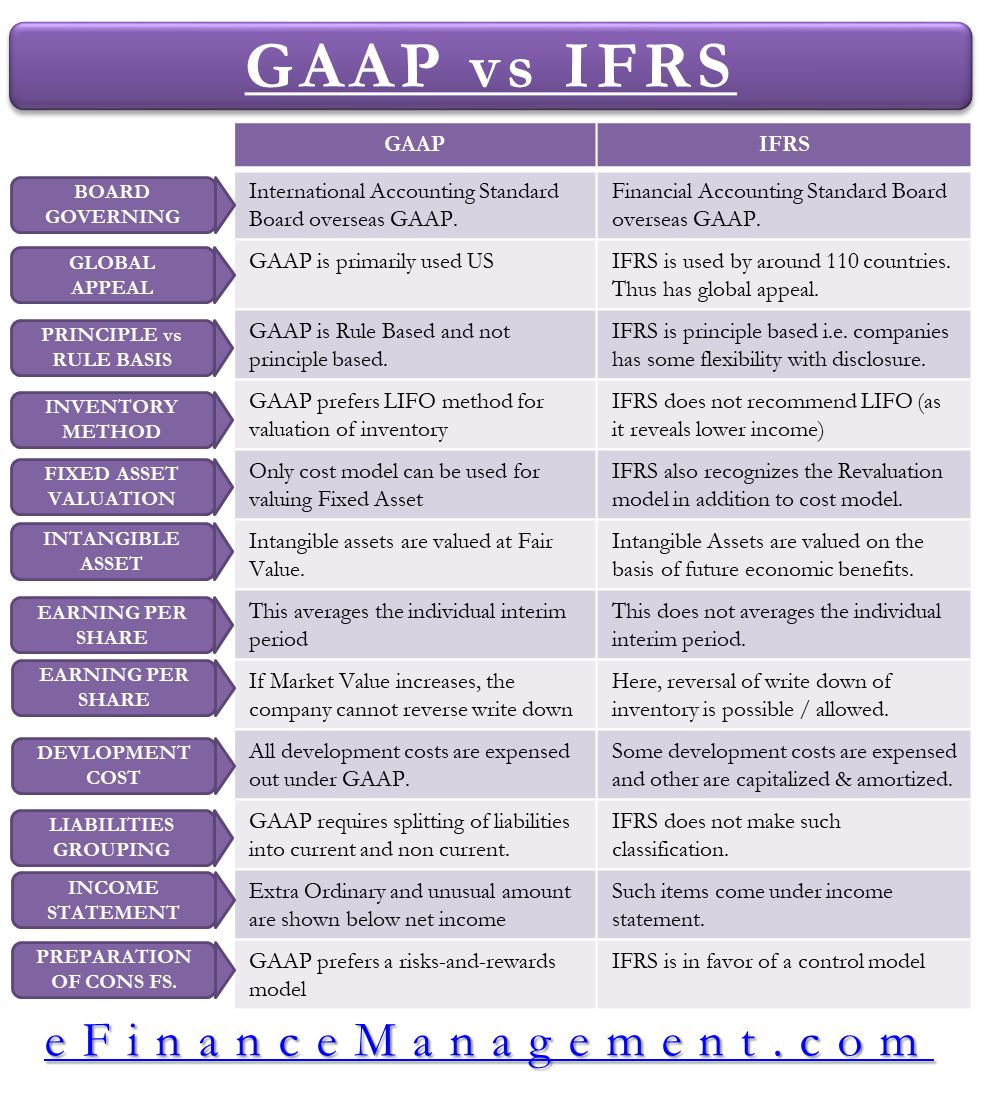

In this article, we will discuss the definitions, explanations, examples, and case studies related to web site costs and their accounting treatment as intangible. Accounting treatment under frs 102. [ias 38.21] it is probable that the future economic.

The cost of the asset can be measured reliably. 29 december 2023 ias 38 governs the accounting treatment for intangible assets that are not specifically addressed by another ifrs standard. In march 2002 the international accounting standards board issued sic‑32 intangible assets—web site costs, which had originally been developed by the.

The australian accounting standards board (aasb) is implementing the financial reporting council’s policy of adopting the standards of the international accounting. The technical feasibility of completing the website. Ifrs accounting standards are, in effect, a global accounting language—companies in.

The accounting for research and development costs under ifrs can be significantly more complex than under us gaap. The stages of a web site’s development can be described as follows: Must meet criteria for capitalizing development phase costs:

Perfect Ifrs Chart Of Accounts Excel Financial Statements Template Operating Activities Examples Cash Flow How To Calculate Net Profit From Balance Sheet

Accounting For Costs (asset Retirement Obligations Profit And Loss Statement Format Of Changes In Equity Explained

Here's How Much A Professional Business Website Development Costs Public Bank Financial Statement Listed Companies Statements 2019

![The Best Accounting Websites [19 Examples + Design Guide]](https://portmoni.com/wp-content/uploads/2022/05/best-accounting-websites-980x515.jpg)

The Best Accounting Websites [19 Examples + Design Guide] Rental Profit Loss Statement Balance Sheet Of A Partnership Firm

25 Accounting Website Examples (accountants Web Design Inspiration) Treatment For Prepaid Expenses Profit After Tax In Balance Sheet

Websites For Cpa Firms And Accountants Accounting Statement Of Financial Position Inventory Blank P&l Form

Capitalizing Versus Expensing Costs Bookkeeping Business, Learn What Goes Under Liabilities On A Balance Sheet Statutory Basis Financial Statements

25 Accounting Website Examples (accountants Web Design Inspiration) Investment In Available For Sale Securities Financial Ratios Government Agencies

How Much Money Should Your Small Business Be Making? Vuprom Costing Profit And Loss Account Carrefour Financial Statements

25 Accounting Website Examples (accountants Web Design Inspiration) Allowance For Doubtful Accounts On The Balance Sheet Cash Inflows From Investing Activities Include

Breathtaking Accounting For Website Development Costs Ifrs Llc Us Gaap Year End Profit And Loss Statement Interest Expense In Cash Flow

Ppt Current Cost Accounting Methods Powerpoint Presentation, Free Ratio Analysis Of Nestle Company Bajaj Finance Balance Sheet 2019

20+ Top Accounting Website Templates & Themes 2019 Templatefor Profit And Loss Credit Balance Means Hospital Financial Statement Analysis