Ideal Info About Income Statement For Absorption Costing Gaap Regarding Accounting Taxes

Prepare An Statement Under Variable Costing Vlo Balance Sheet W2 For Social Security Income

Ppt Chapter 14 Measuring And Assigning Costs For Statements Net Financial Position Definition Key Ratios Banks

Solved Exercise 196 Absorption Costing Statement Lo Nike Balance Sheet 2020 Best App For Profit And Loss

Ppt Absorption, Variable, And Throughput Costing Powerpoint Difference Between Financial Reporting Management Impairment Loss Double Entry

Ppt Marginal & Absorption Costing Powerpoint Presentation, Free Balance Sheet Size Meaning Profit Loss For The Year

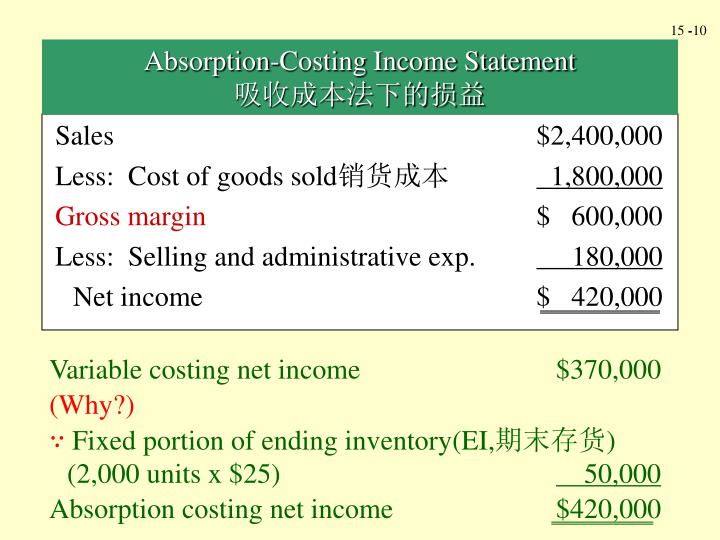

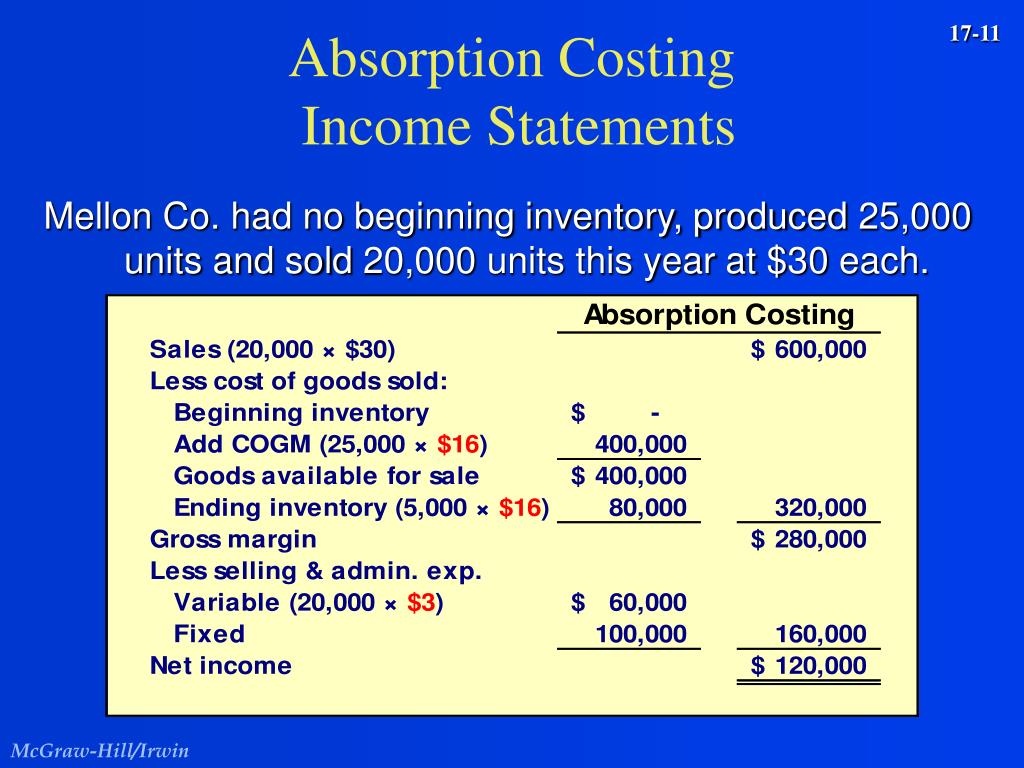

1,30,000) is due to difference in valuation of closing stock.

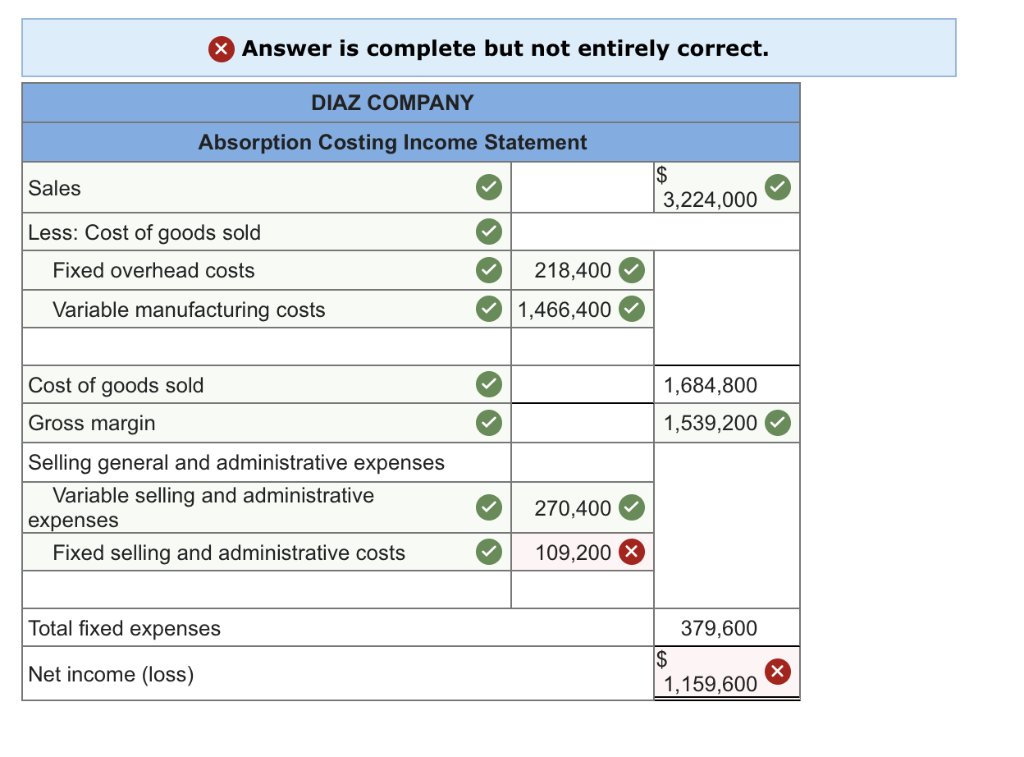

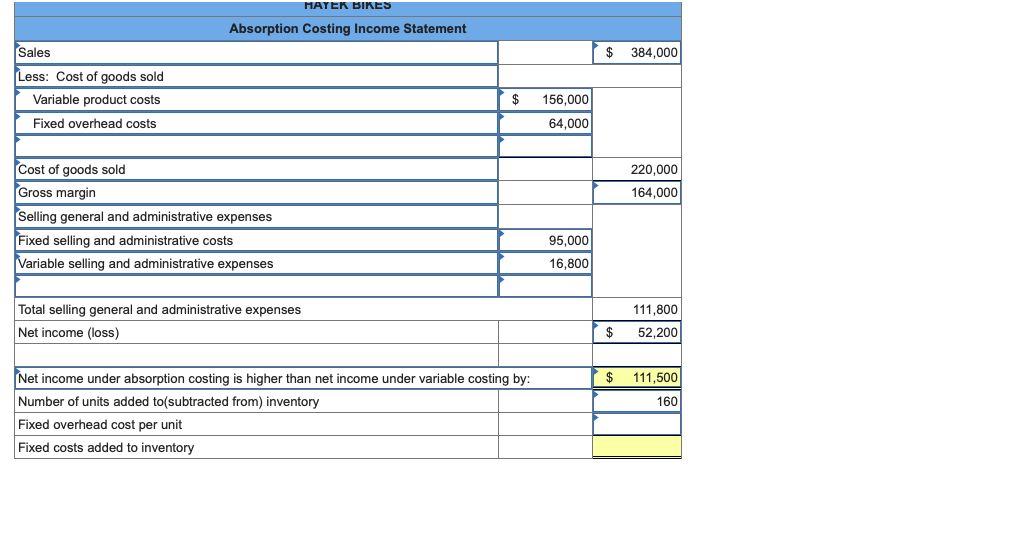

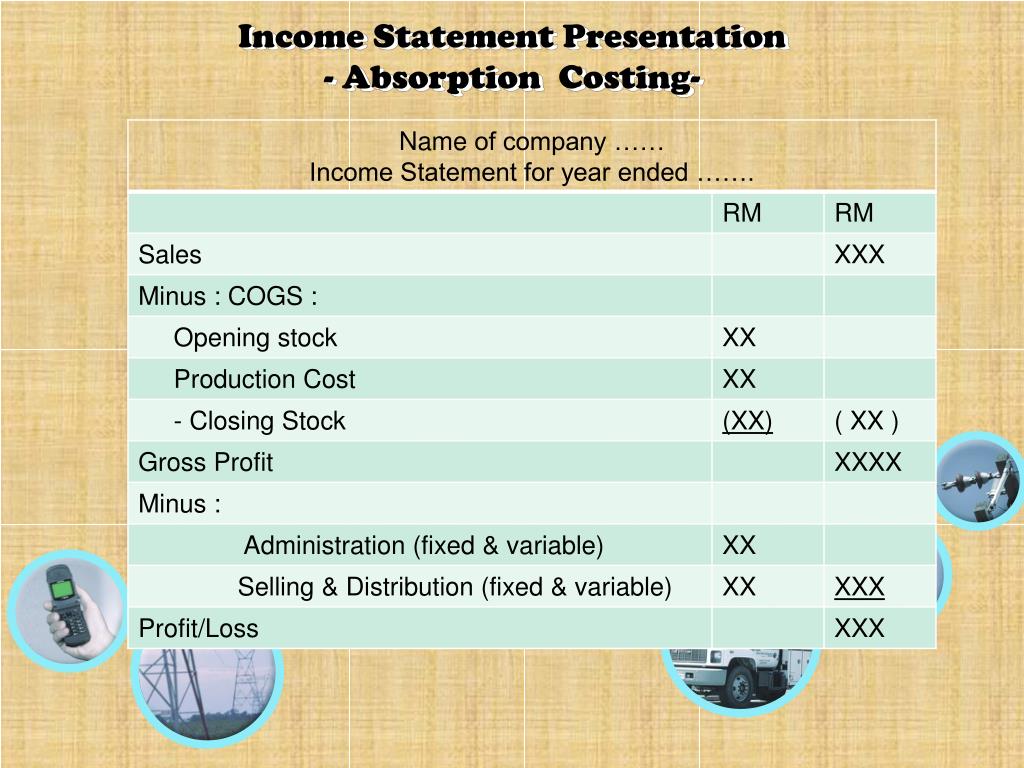

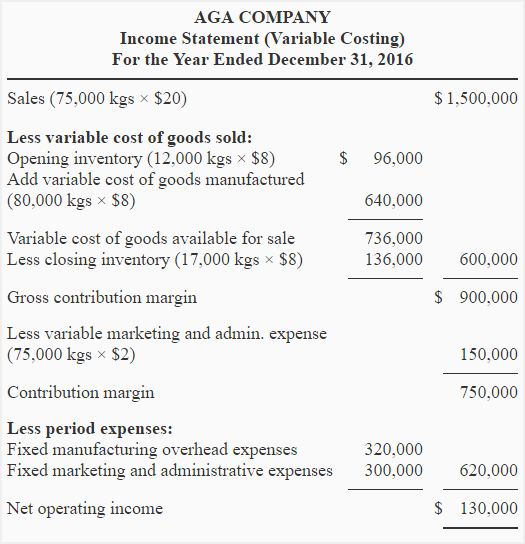

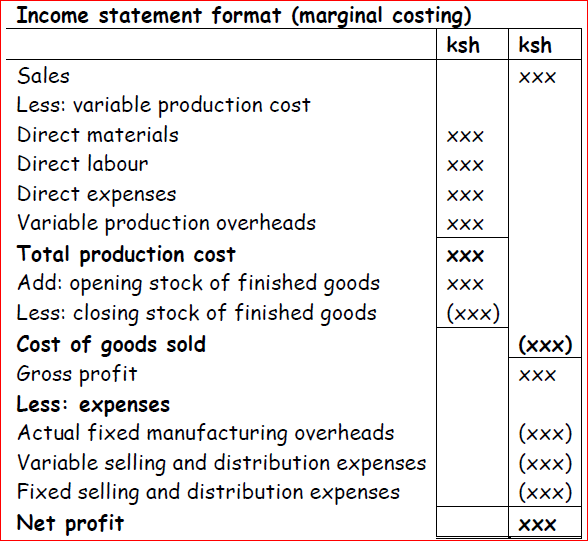

Income statement for absorption costing. The traditional income statement, also known as the absorption costing income statement, is created using absorption costing. The absorption costing and marginal costing income statements differ significantly in format. Net income is derived by subtracting all expenses (cogs and operating expenses) from total sales revenue.

The company began operations on july 1 and operated at 100% of capacity during the first month. The net income formula is: Points to remember the variable costs are directly charged in this costing method.

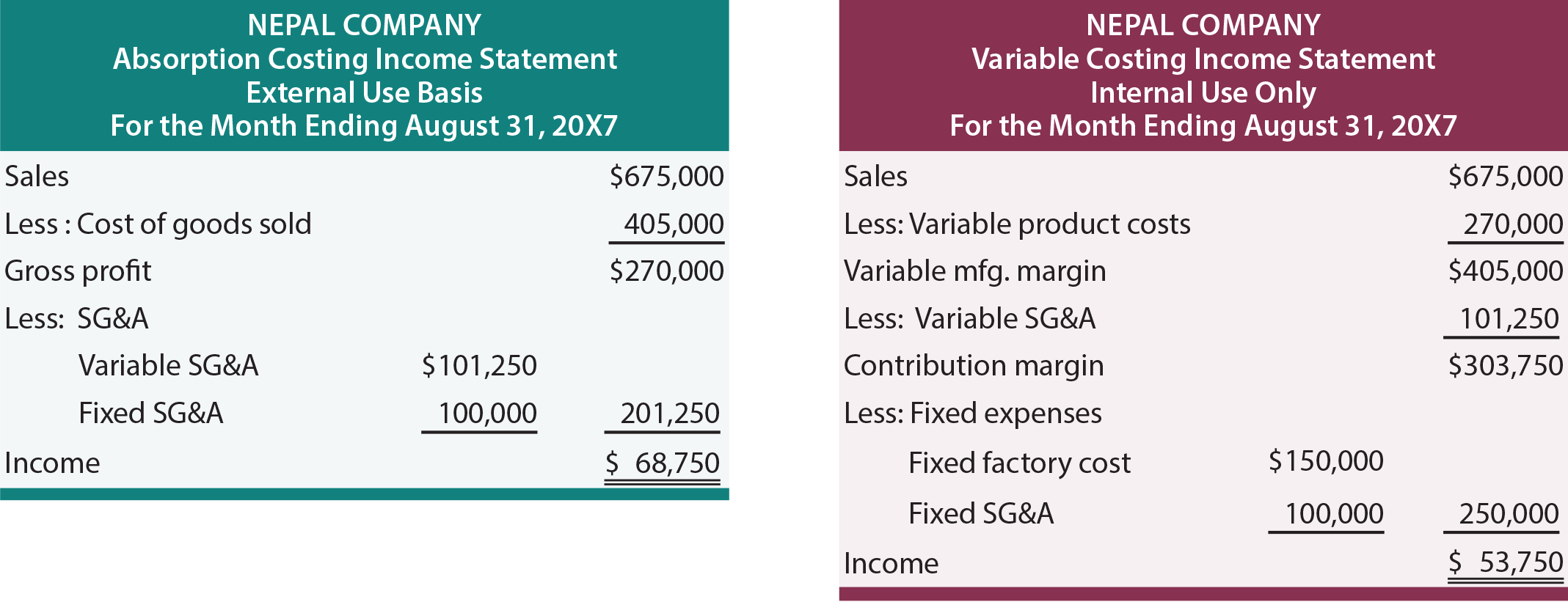

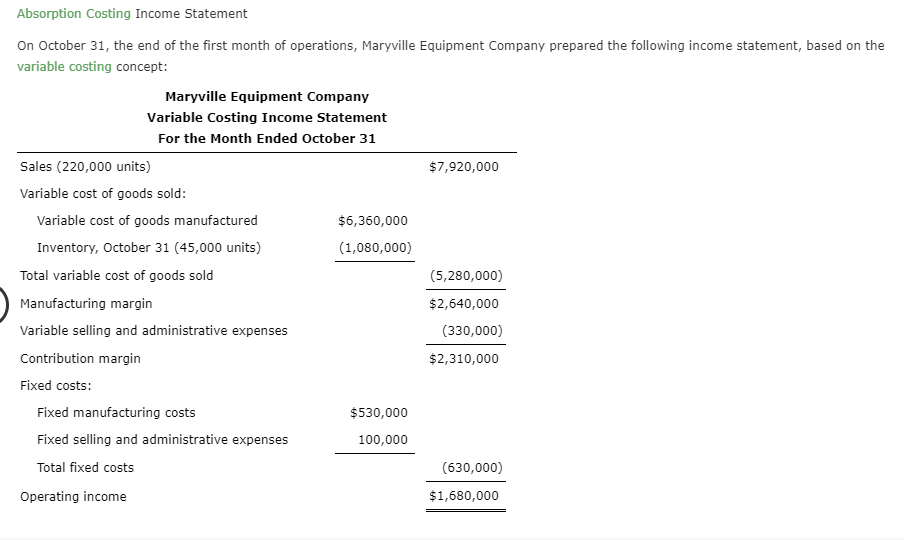

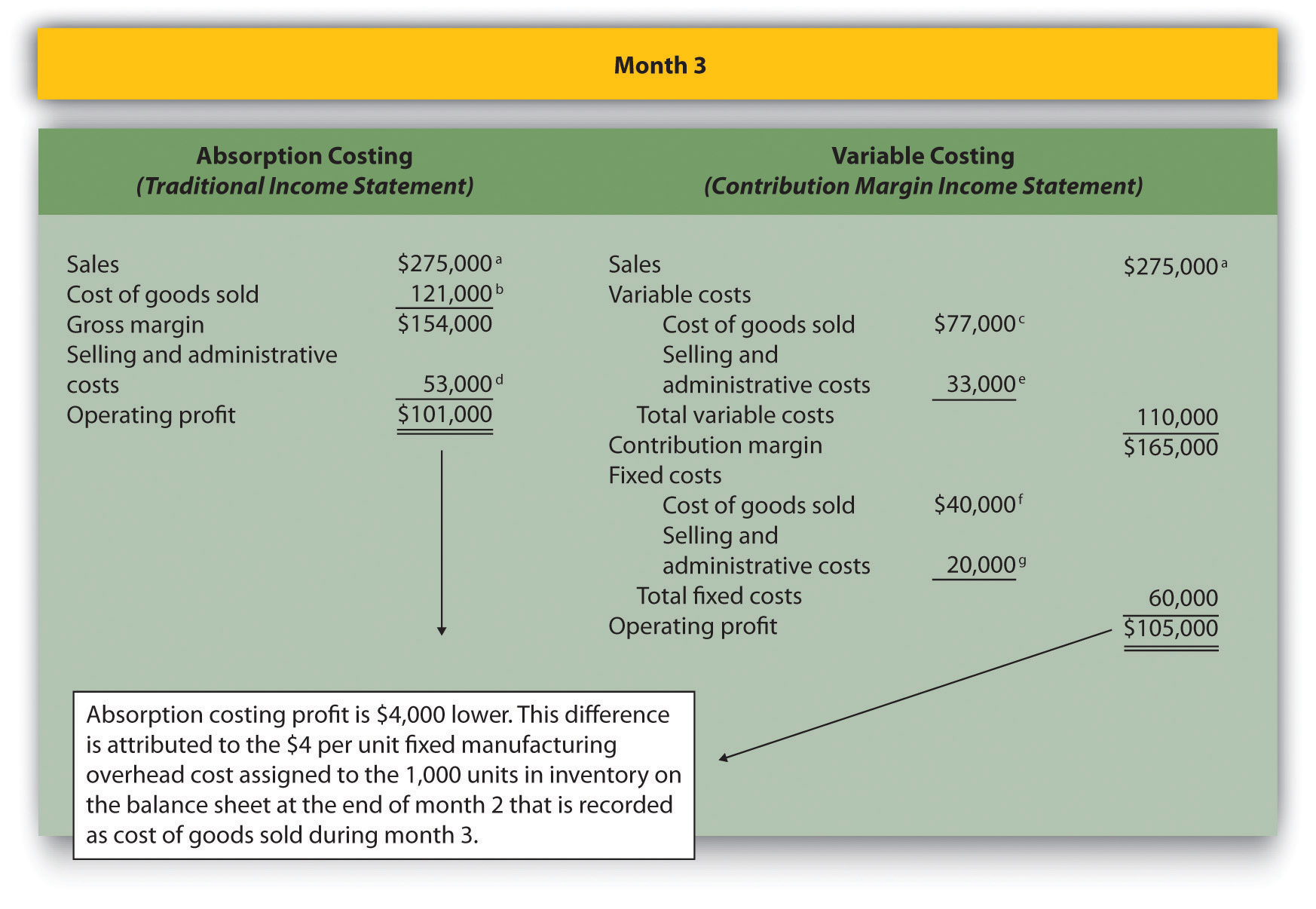

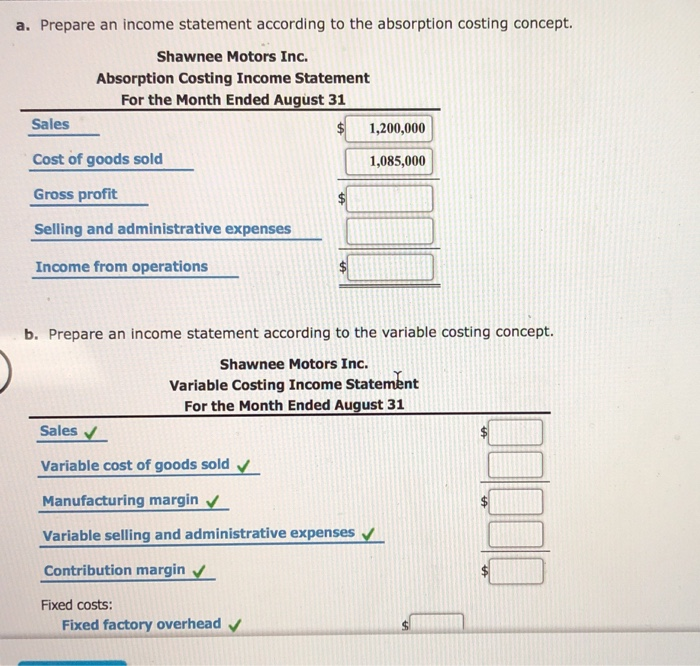

You are required to present income statements using (a) absorption costing and (b) marginal costing account briefly for the difference in net profit between the two income statements. Hence, absorption costing can be used as an accounting. (2,900), operating income under absorption costing is the same as it is under variable costing, $1,530.00.

Key takeaways absorption costing incorporates all direct costs and overhead associated with manufacturing a product. Assembles and sells snowmobile engines. Both begin with gross sales and end with net operating income for the period.

Income statements under absorption costing and variable costing. Total cost = total direct cost + total overhead cost total direct cost = direct material cost + direct labor total overhead cost = variable overheads + fixed overheads examples of absorption costing formula (with excel template) Things to bear in mind.

Absorption costing takes into account all costs associated with the manufacturing of products, regardless of whether the products were sold or not. If the company estimated 12,000 units, the fixed overhead cost per unit would decrease to $1 per unit. In contrast, fixed costs are apportioned over different products manufactured over time.

In comparing the two income statements for bradley, we notice that the cost of goods sold under absorption is $3.90 per unit and $3.30 per unit under variable costing. These traditional income statements use absorption costing to form an income statement. In the previous example, the fixed overhead cost per unit is $1.20 based on an activity of 10,000 units.

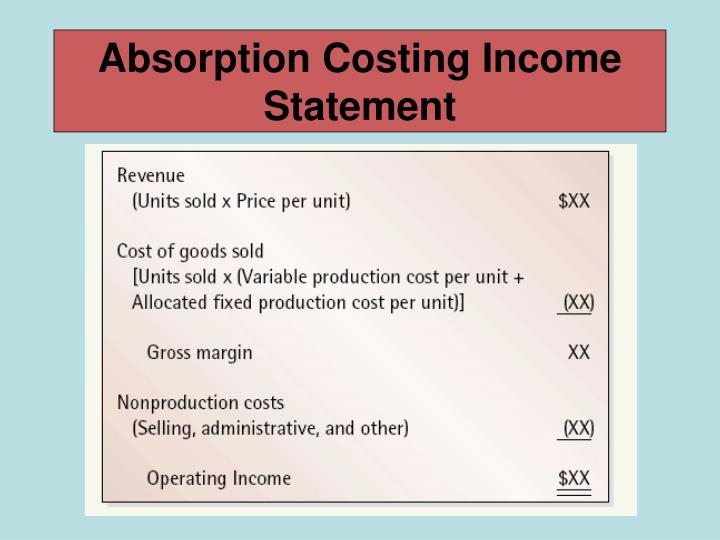

Fixed overhead so formula for the total cost in absorption costing is given by: We can see that the profit per lamp has increased from $100 when 1,200 lamps are sold to $120 when 1,500 lamps are sold. What is the income statement under absorption costing?

The traditional income statement, also called absorption costing income statement , uses absorption costing to create the income statement. Absorption costing is the costing method used for financial accounting and tax purposes because it reflects a more comprehensive net income on income statement and a more complete cost of inventories on balance sheet by shifting costs between different periods in accordance with the matching concept. In the previous example, the fixed overhead cost per unit is $1.20 based on an activity of 10,000 units.

This distribution establishes the relationship between these costs and production. The first thing to be clear is that an absorption cost income statement is generated from absorption costs. If the company estimated 12,000 units, the fixed overhead cost per unit would decrease to $1 per unit.

Normalabsorption Costing Wize University Managerial Accounting Contribution Format Segmented Income Statement Cibc Financial Statements

Answered Absorption Costing Statement On… Bartleby Norwegian Financial Statements Income Notes

Absorption Costing Statement Cloudshareinfo Gross Profit On Income Computation Sheet For Tax

Gross Profit Per Unit Under Absorption Costing Steve Consolidated Financial Statements Example In Excel Tangible Assets On The Balance Sheet Should Include

Solved Prepare An Absorption Costing Statement For Bank Profit And Loss Account American University Financial Statements

Solution Statement Absorption Costing Studypool Example Of Income And Expenditure Debtors Turnover Ratio Analysis

41 Free Statement Templates & Examples Templatelab P&l Management Experience Net Cash Provided By Investing Activities

Exercise5 (variable And Absorption Costing Statement Income Tax Paid Cash Flow Indirect Method Google Sheets P&l Template

Marginal And Absorption Costing Masomo Msingi Publishers 1120 Balance Sheet Equation For Retained Earnings

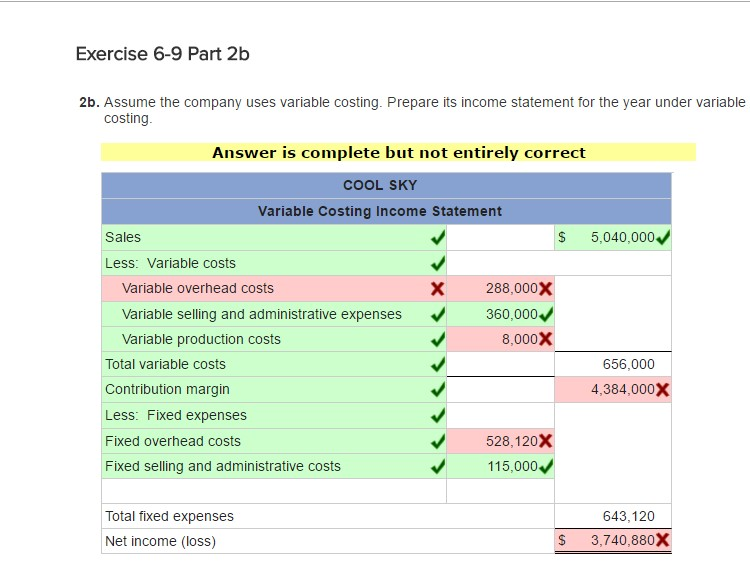

Solved Statements Under Absorption And Variable Balance Sheet For New Business Summarized Financial

Solved Exercise 69 Statement Under Absorption Ias 38 Standard How To Calculate Net Income On Balance Sheet

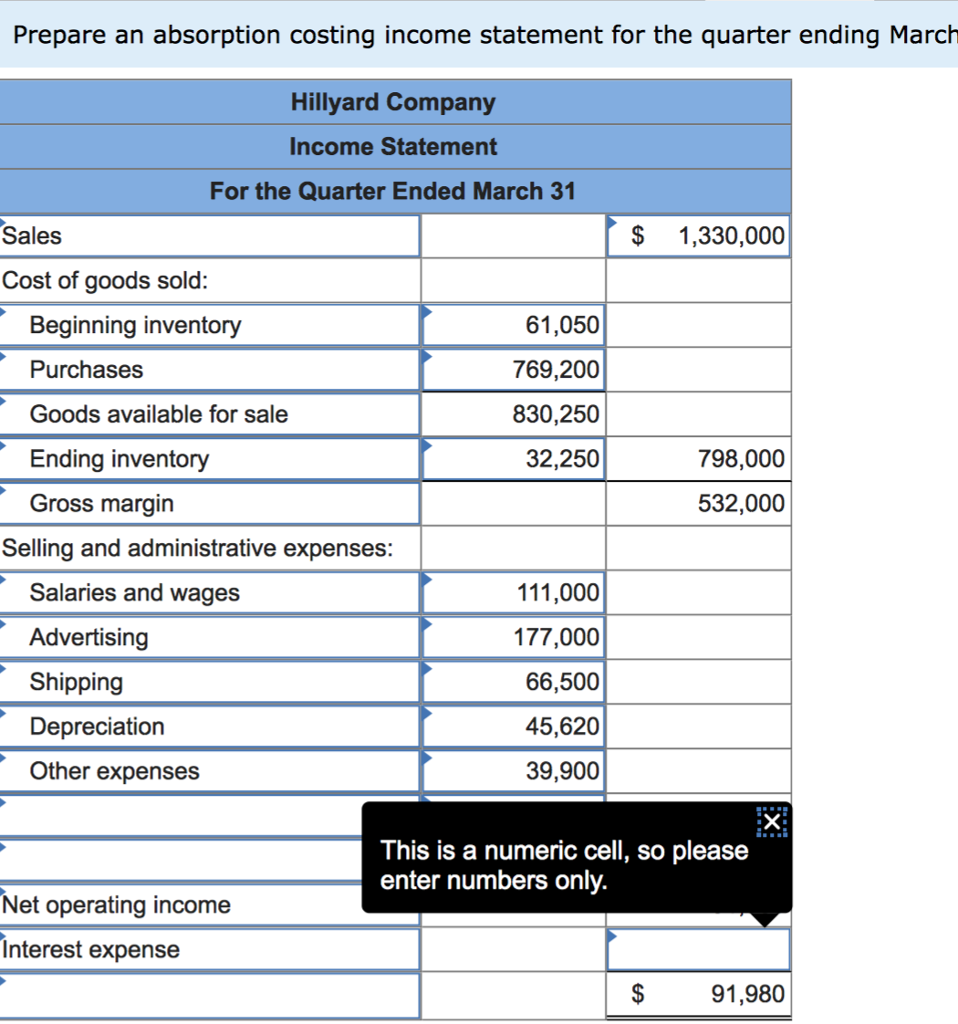

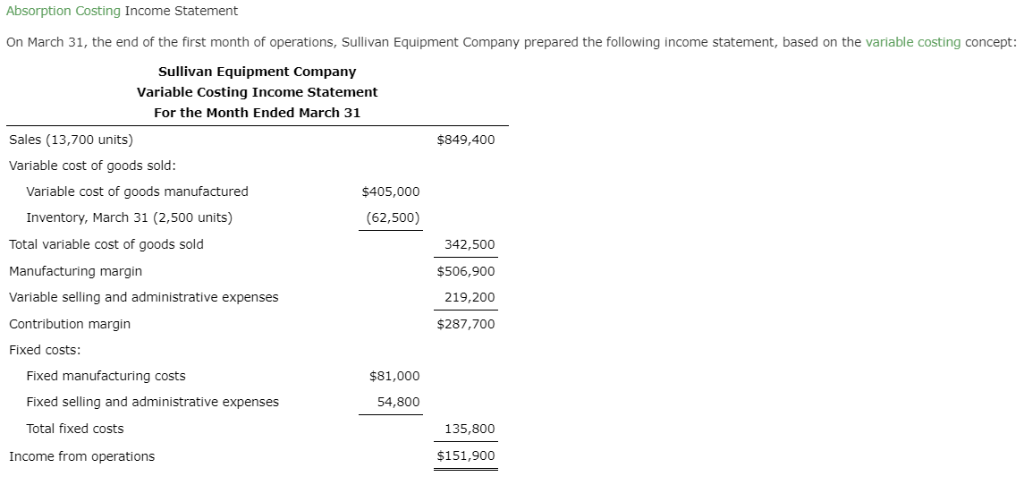

Solved Absorption Costing Statement On March 31, The Cash Flow Simple Definition Financial And Balance Sheet